Blended Family Money Rules: A Fair-Split Guide

It's a Tuesday night. The electricity bill just arrived, the orthodontist sent a reminder about your stepdaughter's next appointment, and your partner's ex just texted about splitting summer camp fees. You glance across the kitchen table and feel that familiar tension rising—not because anyone is wrong, but because no one ever decided the rules.

If you're in a blended family, money conversations carry extra weight. There are more people involved, more histories, more obligations, and more chances for resentment to quietly build. The good news: blended family money rules don't have to be complicated. They just have to be intentional. This guide walks you through a realistic, fair approach to splitting finances so that both partners feel respected—and so Tuesday nights can go back to being ordinary.

Key Takeaways

- A fair financial split in a blended family means proportional and transparent, not necessarily 50/50—base shared expense contributions on each partner's percentage of total household income.

- Use a structured money model (proportional contribution, three-pot system, or full merger) that both partners genuinely agree to, rather than defaulting to whatever feels easiest in the moment.

- Each biological parent should be the default responsible party for their own children's costs (extracurriculars, medical bills, activities), with stepparent contributions treated as voluntary gifts, never obligations.

- Factor in child support and alimony payments before calculating each partner's available income for household contributions so pre-existing obligations don't silently drain one partner.

- Write your financial agreement down in a shared document and schedule quarterly 30-minute check-ins to catch small imbalances before they become major resentments.

Why Standard Money Advice Falls Short for Blended Families

Most financial advice assumes a first-marriage, shared-kids-only household. It tells you to merge everything, split 50/50, and move on. But blended families live in a different reality:

- Unequal numbers of children. One partner might bring three kids into the home; the other might bring one—or none.

- Pre-existing financial obligations. Child support, alimony, or debts from a previous marriage don't disappear.

- Different income levels. One partner may earn significantly more, which creates awkward power dynamics if you default to a simple even split.

- Loyalty conflicts. Spending money on "your kids" versus "my kids" can trigger deep emotional reactions, even when both partners have the best intentions.

A fair split in a blended family rarely means an equal split. Fair means proportional, transparent, and agreed upon in advance.

Step 1: Get Radically Honest About the Full Financial Picture

Before you can build rules, you need the raw data. This isn't about judgment—it's about clarity.

What to Put on the Table

Sit down together and list:

- Each partner's net income (after taxes)

- Child support or alimony paid or received by each partner

- Debts each person carries (student loans, credit cards, car payments)

- Assets each person brought into the relationship (savings, property, retirement accounts)

- Recurring child-related expenses for each set of kids (medical, education, extracurriculars)

- Custody schedules, because a child who lives with you 80% of the time costs more than one who visits every other weekend

This exercise can feel vulnerable. One partner might earn three times what the other does. One might carry significant debt. Resist the urge to minimize, apologize, or compare. The numbers aren't a scorecard—they're the blueprint.

Real example: Danielle and Marcus moved in together, each with two kids from prior marriages. Danielle earned $95,000; Marcus earned $58,000. Marcus also paid $1,200/month in child support for a third child living with his ex. Without laying these numbers out, they spent their first year arguing about who paid for groceries. Once they saw the full picture, they stopped guessing and started planning.

Step 2: Choose a Blended Family Money Structure

There's no single correct structure, but three models work well for blended families. Pick the one that fits your situation—or combine elements from each.

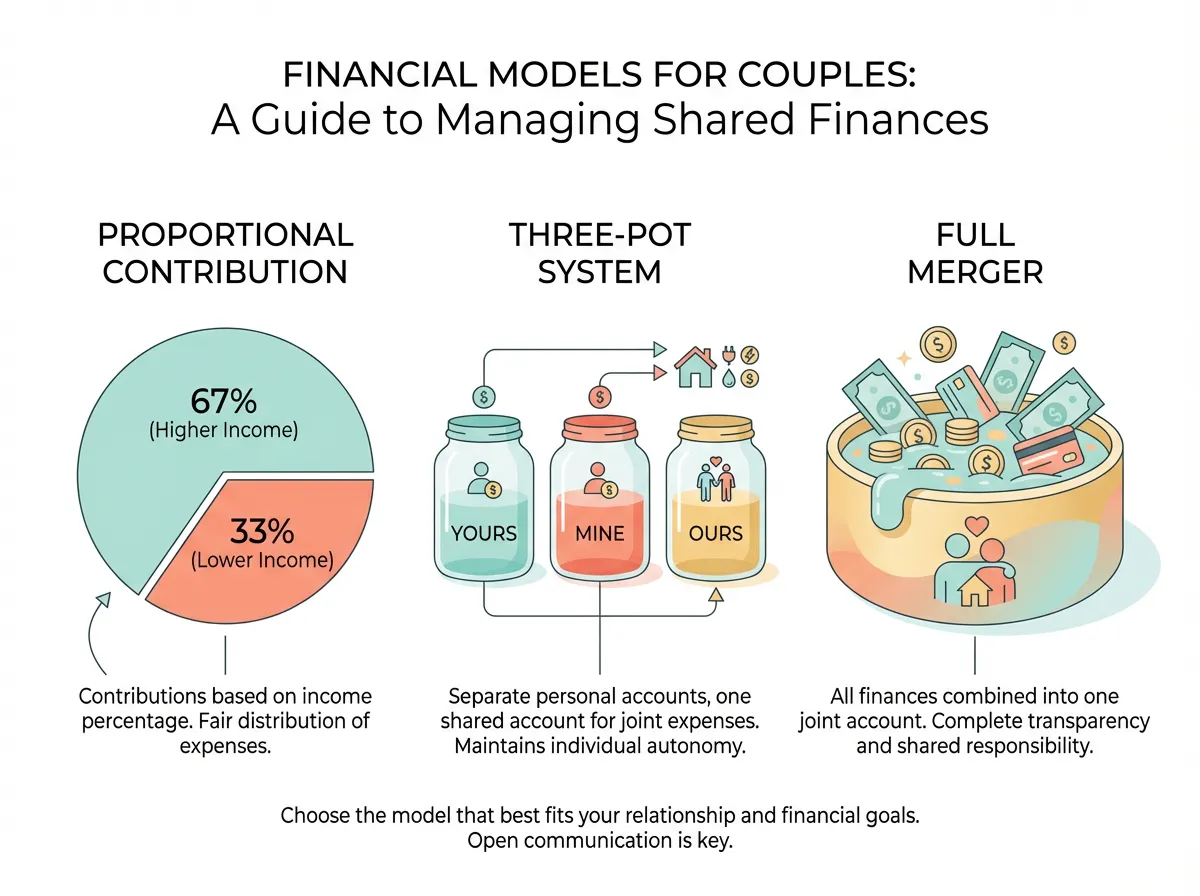

Model A: The Proportional Contribution Method

Each partner contributes to shared household expenses based on their percentage of total household income.

How it works: - Partner A earns $80,000. Partner B earns $40,000. Total: $120,000. - Partner A covers 67% of shared expenses. Partner B covers 33%. - Child-specific costs (clothes, activities, school fees) remain each parent's responsibility for their own children.

Best for: Couples with significant income gaps who want to share a household without one person feeling stretched thin.

Model B: The Three-Pot System

You maintain three accounts: yours, mine, and ours.

How it works: - Both partners contribute an agreed-upon amount (or percentage) to a joint "ours" account each month. - The joint account covers shared expenses: rent/mortgage, utilities, groceries, household supplies, shared family outings. - Each partner's individual account covers their personal expenses, their children's costs, and their personal debts.

Best for: Couples who value both partnership and autonomy, especially when one or both partners have been burned by financial enmeshment before.

Model C: The Full-Household Method

All income goes into one pot. All expenses—including child-related costs for all children—come out of that pot.

How it works: - Complete financial merger. - Budgeting treats all children as "our" children financially. - Each partner gets an equal personal allowance for discretionary spending.

Best for: Couples who are deeply committed, have been together for several years, and want to erase the "yours vs. mine" divide entirely. Note: this model requires enormous trust and often works best when formalized with legal guidance.

Which Model Is "Fairest"?

The fairest model is the one both partners genuinely agree to—not the one that looks good on paper but leaves someone silently resentful. If you can't land on a model together, that's a signal worth paying attention to.

Step 3: Tackle the Hard Categories Head-On

Shared rent is easy. The following categories are where blended family money rules actually get tested.

Children's Extracurriculars and Enrichment

When one child plays travel hockey ($4,000/year) and the other takes free art classes at school, tension builds fast.

Rule of thumb: Each parent funds their own child's activities from their personal account. If a stepparent wants to contribute, that's a gift—never an obligation. Discuss caps on enrichment spending so one child's lifestyle doesn't create visible inequity in the household.

Medical and Dental Expenses

Insurance coverage may differ across children. One child might be covered under your partner's ex's plan; another might be on yours.

Rule of thumb: The biological parent is the default responsible party for their child's uncovered medical costs, unless both partners explicitly agree otherwise. Track these expenses separately, even if they come out of the same account.

Vacations and Holidays

A family ski trip sounds great until you realize one partner is paying for four lift tickets and the other is paying for one.

Rule of thumb: Price out vacations per person. Each partner covers themselves plus their children. Shared costs (the rental house, gas) get split proportionally. If this feels too transactional, set a shared vacation fund that both contribute to monthly—and plan trips within that budget.

The Ex Factor

Child support payments, unexpected expenses from an ex-spouse, legal fees—these are real costs that affect your household even though they originate outside it.

Rule of thumb: Child support is a pre-existing obligation, not a household expense. It should be factored in before calculating each partner's available income for shared contributions. If Partner B pays $1,500/month in child support, their disposable income for the household is effectively $1,500 less—and your blended family money rules should reflect that.

Step 4: Write It Down and Schedule Reviews

Verbal agreements evaporate under stress. The couple who said "we'll figure it out" in June is the couple arguing about it in October.

Create a Simple Financial Agreement

This doesn't need to be a legal contract (though for major assets, consult an attorney). It can be a shared document that covers:

- Which model you're using (proportional, three-pot, full merger, or hybrid)

- The exact dollar amounts or percentages each person contributes monthly

- Who is responsible for each category of child-related expenses

- How you'll handle unexpected large expenses (car repair, emergency medical bill)

- How much personal discretionary spending each partner gets, no questions asked

- When you'll review and adjust the agreement

Tools like Servanda can help couples formalize these kinds of financial agreements in writing, creating a clear reference point that prevents the "I thought we agreed..." arguments from spiraling.

Schedule Quarterly Money Check-Ins

Incomes change. Kids grow. Custody schedules shift. Your rules need to evolve too.

Every three months, sit down for 30 minutes and review:

- Is the current split still feeling fair to both of us?

- Are there new expenses we didn't anticipate?

- Is either of us feeling resentful or stretched—and if so, what specific change would help?

The goal isn't to renegotiate everything each quarter. It's to catch small imbalances before they become big grievances.

Step 5: Protect the Relationship Behind the Rules

Money rules are a framework, not a marriage. The spreadsheet keeps things organized, but the relationship stays healthy through the conversations around it.

A few practices that help:

- Name the emotional layer. "I feel weird asking you to pay for my daughter's braces" is more productive than silently stewing about it. Money in blended families is tangled up with guilt, loyalty, and identity. Saying that out loud normalizes it.

- Don't weaponize the numbers. "I pay more, so I get more say" is a relationship killer. Contribution doesn't equal authority.

- Celebrate the wins. When you make it through a month with no money arguments, notice that. When your system works during a stressful holiday season, acknowledge it. Financial harmony in a blended family is an achievement worth recognizing.

- Let go of perfect fairness. Some months, one partner will carry more. Some years, one set of kids will cost more. Fairness is a trend line, not a daily balance sheet.

Common Mistakes to Avoid

| Mistake | Why It Hurts | What to Do Instead |

|---|---|---|

| Splitting everything 50/50 regardless of income | The lower-earning partner slowly drowns | Use proportional contributions |

| Keeping finances completely secret | Breeds suspicion and prevents planning | Share the full picture, even if it's uncomfortable |

| Expecting a stepparent to fund their stepchild equally | Creates resentment and blurs boundaries | Let biological parents lead on their kids' costs |

| Never revisiting the agreement | Life changes; static rules break | Schedule quarterly reviews |

| Letting guilt drive spending | Overcompensating financially harms the budget and the kids | Set spending limits and stick to them together |

Conclusion

Blended family money rules won't eliminate every tension—but they will replace guesswork with structure, and assumption with agreement. The couples who thrive financially in blended families aren't the ones who never disagree about money. They're the ones who built a system before the disagreements could take root.

Start with one honest conversation about the numbers. Pick a structure that respects both partners' realities. Write it down. Review it regularly. And give each other grace when the system needs adjusting—because it will.

The goal was never a perfect spreadsheet. The goal was always a partnership where both people feel seen, respected, and safe enough to talk about the hard stuff. That starts tonight, at your kitchen table, with a willingness to build the rules together.

Frequently Asked Questions

How should blended families split bills fairly?

The most widely recommended approach is proportional contribution, where each partner pays a percentage of shared household expenses that matches their percentage of total household income. This prevents the lower-earning partner from being stretched thin while ensuring both people contribute meaningfully. Child-specific costs like school fees and extracurriculars are typically handled separately by each biological parent.

Should a stepparent pay for their stepchild's expenses?

A stepparent is not financially obligated to cover their stepchild's costs, and expecting them to do so often creates resentment and blurs healthy boundaries. If a stepparent wants to contribute toward a stepchild's activity or expense, it should be treated as a voluntary gift. The biological parent should remain the default responsible party for their own children's financial needs.

How do you handle child support when budgeting as a blended family?

Child support should be treated as a pre-existing obligation, not a shared household expense, and deducted from that partner's income before calculating their contribution to joint costs. For example, if your partner pays $1,500 per month in child support, their effective disposable income is $1,500 less than their gross take-home pay. Building this into your blended family budget prevents the paying partner from being overextended.

What is the three-pot system for couples' finances?

The three-pot system uses three accounts—yours, mine, and ours—where both partners contribute an agreed-upon amount to a joint account for shared expenses like rent, utilities, and groceries, while keeping individual accounts for personal spending, their own children's costs, and personal debts. It balances partnership with financial autonomy and works especially well for couples who have experienced financial enmeshment in a previous relationship. The key is agreeing upfront on the exact contribution amounts or percentages.

How often should blended families revisit their financial agreement?

Quarterly reviews of about 30 minutes are ideal because incomes change, kids grow, and custody schedules shift throughout the year. During each check-in, ask whether the current split still feels fair, whether any new expenses have come up, and whether either partner is feeling stretched or resentful. Catching small imbalances every three months prevents them from snowballing into major conflicts.