Money Fights in Relationships: How to Stop Them

It's Tuesday night. One of you opens the credit card statement, and the air in the room shifts. Maybe it's a $300 charge at a sporting goods store. Maybe it's another subscription service quietly draining $49 a month. Nobody raises their voice — not yet — but you can feel the script loading: "Why didn't you tell me?" followed by "Why do I have to ask permission?"

If this sounds familiar, you're far from alone. Research consistently places money fights in relationships among the top three sources of recurring conflict between partners, and multiple studies — including landmark work by Sonya Britt-Lutter at Kansas State University — have identified financial disagreements as one of the strongest predictors of divorce, regardless of income level. The issue is rarely the dollar amount. It's what money represents: security, freedom, control, identity.

The good news? You don't need to merge into a single financial mind. You need a shared operating system — a set of agreements, habits, and conversations that let two people with different money wiring live together without resentment. This guide will show you how to build one.

Key Takeaways

- Share your individual money stories with each other to understand the emotional roots behind spending and saving habits, which reduces blame and defensiveness.

- Separate financial values from tactics — most couples actually share the same core values but fight over different strategies to achieve them.

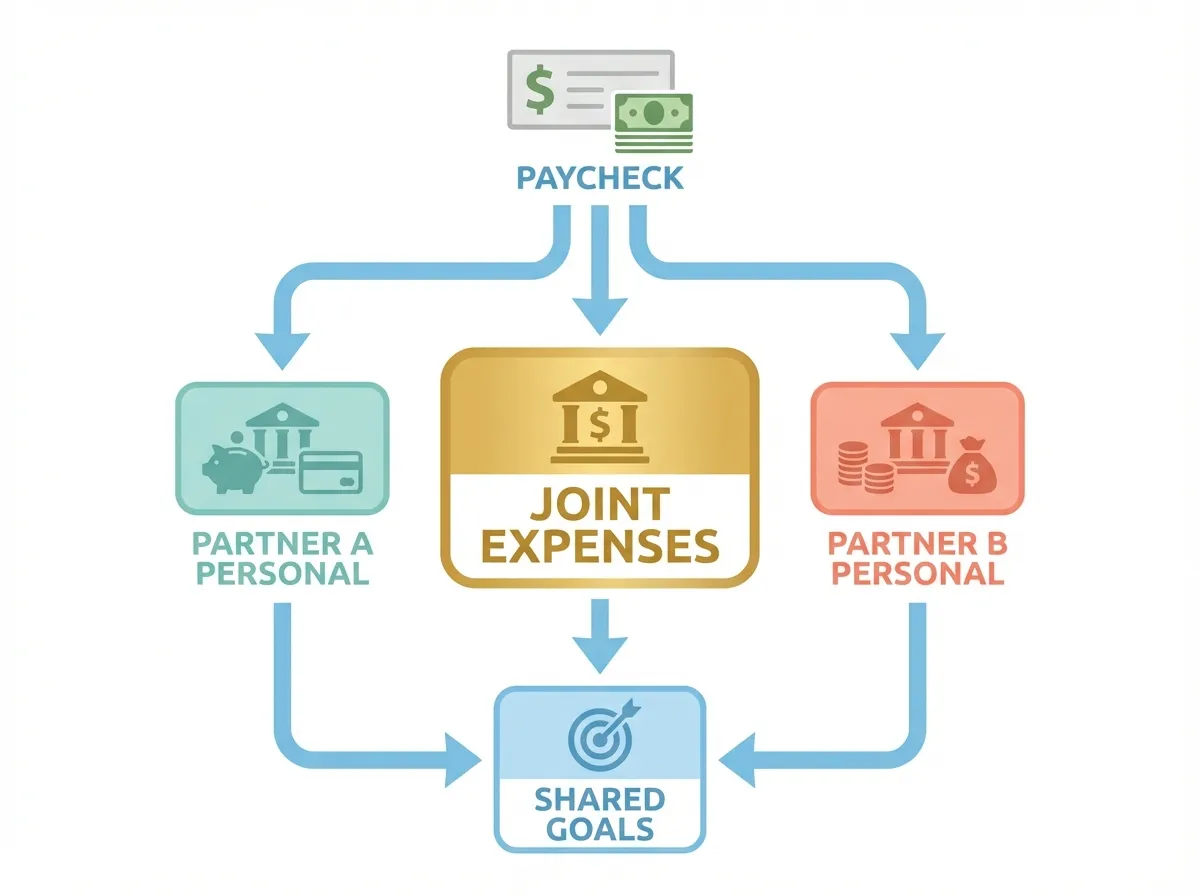

- Use a three-account system (joint expenses, individual spending, shared goals) to balance togetherness with personal autonomy and eliminate the need to ask "permission" to spend.

- Schedule a 30-minute monthly money meeting that starts with wins and uses "I" language to prevent financial stress from leaking into everyday interactions.

- When incomes differ, contribute proportionally (not equally) to shared expenses and explicitly value unpaid labor to prevent hidden power imbalances.

Why Money Fights Feel So Much Worse Than Other Arguments

Arguments about dishes or screen time can sting, but they tend to stay in the present. Money fights pull in the past ("You've always been reckless") and the future ("How will we ever retire?") simultaneously. That's what makes them so exhausting.

The Hidden Layers Beneath Every Dollar Dispute

Most financial arguments are proxy wars. Beneath the surface-level disagreement — "You spent too much" or "You're too cheap" — deeper concerns are almost always at play:

- Security vs. freedom: One partner treats savings as a safety net; the other sees unspent money as unlived life.

- Control and autonomy: Earning disparities can create unspoken power dynamics where one person feels they have more "say."

- Family blueprints: If your parents fought about money, you may have internalized either hyper-vigilance or avoidance around finances — both of which confuse your partner.

- Shame and identity: Debt, low income, or financial mistakes carry enormous stigma. Defensiveness often masks embarrassment.

Until you name these underlying currents, you'll keep arguing about the credit card bill without ever solving anything.

Step 1: Map Your Individual Money Stories

Before you can align financially as a couple, each person needs to understand their own relationship with money. This isn't therapy homework — it's a 20-minute conversation that can prevent years of recurring conflict.

Sit down separately and answer these questions in writing:

- What did money mean in your household growing up? (Scarcity? Status? A taboo topic?)

- What's your earliest money memory that carries an emotional charge?

- When you imagine financial safety, what does the picture look like? (A specific number in savings? Owning a home outright? Having no debt?)

- What purchase or spending category brings you the most joy — and the most guilt?

Then share your answers with each other. The goal isn't to debate. It's to listen. When you understand that your partner's frugality comes from watching their parents lose a home, or that your partner's generosity is how they express love, the same behaviors that used to trigger you start making sense.

A Real-World Example

Consider a couple — let's call them Mia and James. Mia grew up in a household where money was openly discussed and budgeted down to the dollar. James's family never talked about money at all; his parents simply bought what they wanted and dealt with consequences later. In their marriage, Mia's spreadsheets felt controlling to James, and James's spontaneous purchases felt reckless to Mia. Neither was wrong. They were running on different operating systems. Once they articulated their money stories to each other, the emotional charge around their disagreements dropped significantly — not because they suddenly agreed, but because they stopped attributing motive to behavior.

Step 2: Separate "Values" from "Tactics"

Couples often think they disagree about values when they actually disagree about tactics. This distinction is critical.

- Value: "We want to feel financially secure."

- Tactic: "We should keep $30,000 in an emergency fund" vs. "We should invest aggressively so our money grows."

Both tactics serve the same value. Once you realize that, negotiation becomes possible.

Try this exercise together:

- Each of you writes down your top five financial values (e.g., security, generosity, experiences, independence, legacy).

- Compare lists. You'll likely share at least three.

- For each shared value, brainstorm multiple tactics that could satisfy it.

This reframes the conversation from "you're wrong" to "how else could we get what we both want?"

Step 3: Design a Money System That Respects Both Partners

Abstract agreement is easy. The hard part is building a day-to-day system that actually works. Here's a framework used by financial therapists that you can adapt to your situation.

The Three-Account Structure

Instead of arguing about whether to combine finances or keep them separate — a debate with no universally correct answer — consider a hybrid model:

- Joint account for shared expenses: Mortgage or rent, utilities, groceries, childcare, insurance, joint savings goals. Both partners contribute a proportional percentage of their income (not a flat dollar amount — this matters when incomes differ).

- Individual accounts for personal spending: Each person gets a set amount every month that is theirs to spend, save, or burn without justification. This is non-negotiable autonomy.

- Joint savings/investment account for shared goals: Vacation fund, house down payment, retirement contributions beyond employer matches.

The individual accounts are the secret weapon. They eliminate the single most corrosive dynamic in couples' finances: the feeling that you need permission to spend your own money.

Set a "Notification Threshold" — Not a Permission Threshold

Agree on a dollar amount above which you'll inform each other before purchasing — not ask permission, but give a heads-up. For most couples, something between $100 and $500 works. Frame it as courtesy, not control.

Automate Where Possible

The fewer financial decisions you have to make together on a daily basis, the fewer opportunities for friction. Set up automatic transfers to each account on payday. Automate bill payments. Automate savings contributions. Reserve your joint mental energy for the big decisions.

Step 4: Hold a Monthly Money Meeting (That Doesn't Feel Like a Tribunal)

Many couples avoid talking about money until something goes wrong — and by then, the conversation is already emotionally charged. A monthly money meeting prevents that buildup.

Here's how to make it bearable:

- Schedule it: Same day each month. Put it on the calendar like a recurring date.

- Keep it short: 30 minutes, max. Use a timer if you need to.

- Start with wins: What went well this month? Did you hit a savings target? Stay under budget on dining out? Acknowledge progress first.

- Review the numbers together: Look at joint account spending, progress toward goals, and any upcoming large expenses.

- Raise concerns with "I" language: "I felt anxious when I saw the balance drop below $2,000" is productive. "You spent too much again" is not.

- End with one action item each: Something small and specific for the next month.

The meeting itself isn't magic. What's magic is that it creates a container for money conversations, so financial anxiety doesn't leak into every other interaction.

Step 5: Build Fair Agreements Around Income Gaps

Income disparity is one of the most underestimated sources of money fights in relationships. When one partner earns significantly more, subtle power imbalances can develop — even between people with the best intentions.

Some principles that help:

- Contribute proportionally, not equally. If one partner earns 70% of the household income, they contribute 70% to shared expenses. Equal percentage means equal sacrifice.

- Value unpaid labor explicitly. If one partner manages the household, provides childcare, or supports the other's career in non-monetary ways, name that contribution out loud and build it into how you think about "who earns what."

- Never weaponize income. The moment someone says "It's my money" in an argument, trust erodes. If you've committed to a partnership, the income belongs to the partnership — even if the accounts are separate.

- Revisit the arrangement when circumstances change. Job loss, parental leave, career pivots — these are moments to renegotiate, not moments to keep score.

Consider formalizing your financial agreements with a tool like Servanda, especially during transitions. Writing down what you've agreed to — contribution percentages, spending thresholds, savings targets — removes ambiguity and gives both partners something concrete to refer back to when emotions cloud memory.

Step 6: Know When Money Fights Aren't Really About Money

Sometimes, no framework will solve the problem because the problem isn't actually financial. Money fights can be a symptom of:

- Eroded trust: Secret spending, hidden debt, or financial infidelity (yes, that's a real term used by therapists) signals a breach that budgeting can't fix.

- Unprocessed resentment: If you're angry about something else — the division of household labor, a career sacrifice, an unresolved betrayal — money becomes a convenient battlefield.

- Mental health struggles: Compulsive spending, financial anxiety, or hoarding behaviors may require professional support beyond what a couple can address on their own.

If your money conversations consistently escalate despite good-faith efforts, a financial therapist (yes, that's a specific specialization) can help. They sit at the intersection of financial planning and couples therapy and are trained to untangle exactly these knots.

What Financial Alignment Actually Looks Like

It's worth naming what success is — and what it isn't.

Financial alignment does not mean: - You agree on every purchase - You have identical financial personalities - You never feel tension about money

Financial alignment does mean: - You have a shared system that both partners helped design - You each have autonomy within agreed-upon boundaries - You have a regular, low-drama venue for money conversations - You understand why your partner relates to money the way they do - You can disagree about a financial decision without questioning each other's character

That last point is the most important. The goal isn't to eliminate disagreement. It's to make disagreement safe — to separate the financial decision from the person making it.

Conclusion

Money fights in relationships persist not because couples are bad at math, but because money is tangled up in identity, security, power, and love. The path forward isn't a perfect budget — it's a set of shared structures and agreements that honor both partners' needs.

Start this week. Share your money stories with each other. Identify one shared value you've been pursuing with conflicting tactics. Set up the three-account structure. Schedule your first 30-minute money meeting.

None of these steps require you to become someone you're not. They require you to build a system that lets you both be who you are — together. The couples who stop fighting about money aren't the ones who finally agree on everything. They're the ones who finally agree on how to disagree.

Frequently Asked Questions

Why do couples fight about money more than anything else?

Money fights are so intense because money is rarely just about dollars — it represents deeply held feelings about security, freedom, control, and identity. Unlike arguments about chores, financial disagreements pull in fears about the past and the future simultaneously, making them feel higher-stakes. Research from Kansas State University has identified financial disagreements as one of the strongest predictors of divorce, regardless of how much a couple earns.

Should couples combine finances or keep them separate?

There's no single right answer, but many financial therapists recommend a hybrid approach: a joint account for shared expenses, individual accounts for personal spending, and a shared savings account for mutual goals. This structure gives both partners autonomy over day-to-day spending while ensuring shared responsibilities and future plans are funded together.

How do you talk about money with your partner without starting a fight?

Start by scheduling a regular, short money meeting — ideally 30 minutes once a month — so conversations happen proactively rather than in moments of frustration. Begin each meeting by acknowledging what went well, use "I" statements to express concerns (e.g., "I felt anxious" instead of "You overspent"), and end with one small, specific action item each.

What is financial infidelity and how do you handle it?

Financial infidelity refers to secretly hiding debt, accounts, or spending from your partner, and therapists treat it as a genuine breach of trust. If you discover hidden financial behavior, budgeting tools alone won't fix the underlying issue — it's a sign to seek help from a financial therapist who specializes in the intersection of money and relationships.

How should couples handle money when one partner earns a lot more?

The most equitable approach is to contribute proportionally to shared expenses based on each partner's income percentage, so the financial sacrifice feels equal. It's also important to explicitly acknowledge unpaid contributions like childcare or household management, and to never use earning power as leverage in an argument, since doing so quickly erodes trust and partnership.