Should You Merge Finances? A Newlywed Checklist

It's three weeks after the honeymoon. You're standing in the kitchen, staring at a credit card bill you didn't expect, and your spouse is asking why you spent $200 on a gadget they've never seen. Suddenly, the glow of the wedding feels very far away.

The question of whether to merge finances hits nearly every newlywed couple, and it rarely arrives as a calm, scheduled conversation. Instead, it shows up disguised as tension over a grocery bill, a whispered worry about student loans, or an awkward silence when one partner earns significantly more than the other. According to a 2024 survey by the Institute for Divorce Financial Analysts, financial disagreements remain one of the top three predictors of divorce.

This newlywed checklist will walk you through the real decisions behind merging finances — not just "should we get a joint account?" but the deeper questions most couples skip until the arguments start.

Key Takeaways

- Before choosing an account structure, have a values conversation about what money meant in each of your families and what financial safety feels like to each of you.

- Use a hybrid "yours, mine, ours" account model with income-proportional contributions to balance autonomy and partnership, especially when there's an income gap.

- Set a specific dollar threshold (e.g., $150) above which either partner checks in before making a purchase — this builds transparency without feeling like permission.

- Write down every financial agreement you make — including how to handle pre-marriage debt — because memory is unreliable and resentment grows in the gaps between what each person remembers.

- Build a financial calendar with weekly, monthly, quarterly, and annual check-ins so money conversations happen on a schedule rather than only when there's a problem.

Why "Should We Merge Finances?" Is the Wrong First Question

Most newlyweds frame this as a binary choice: merge everything or keep everything separate. That framing is the problem. Money in a marriage isn't a light switch; it's a series of dials. You can combine some things, separate others, and adjust over time.

Before you decide what accounts to open, you need to understand what money actually means to each of you. For one partner, a shared account might represent trust and unity. For the other, it might feel like surveillance. Neither interpretation is wrong — but if you don't surface them, you'll end up fighting about a bank account when you're really fighting about autonomy.

Start Here: The Values Conversation

Sit down — not during a bill-paying session, not after a purchase — and ask each other these questions:

- What did money look like in the home you grew up in? Was it openly discussed, or a source of tension? Did one parent control it?

- When do you feel most financially safe? Having savings? Having freedom to spend? Owning assets?

- What purchase would you never want to have to ask permission for?

- What's a financial goal that matters deeply to you — even if it doesn't seem "practical"?

These questions aren't about budgets. They're about understanding the emotional architecture behind your partner's relationship with money. Skip this step, and every financial decision you make together will carry invisible weight.

The Newlywed Merge-Finances Checklist

Here's the practical part. Work through each item together — ideally over two or three short conversations, not one marathon session.

1. Lay Everything on the Table (Literally)

Before you decide how to combine anything, each partner needs to share a complete financial picture. This is the step most couples rush through or avoid entirely, especially when there's shame involved.

Create a shared document with:

- Income: Salary, freelance earnings, side income, expected bonuses

- Debts: Student loans, credit cards, car payments, medical debt, personal loans

- Assets: Savings, investments, retirement accounts, property

- Credit scores: Pull them together; no surprises

- Recurring obligations: Alimony, child support, family financial support

Real-world example: Priya and James avoided this conversation for six months after their wedding. When Priya finally admitted she had $38,000 in student debt, James didn't react the way she feared — he was hurt she hadn't trusted him with it sooner. The debt wasn't the problem. The secrecy was.

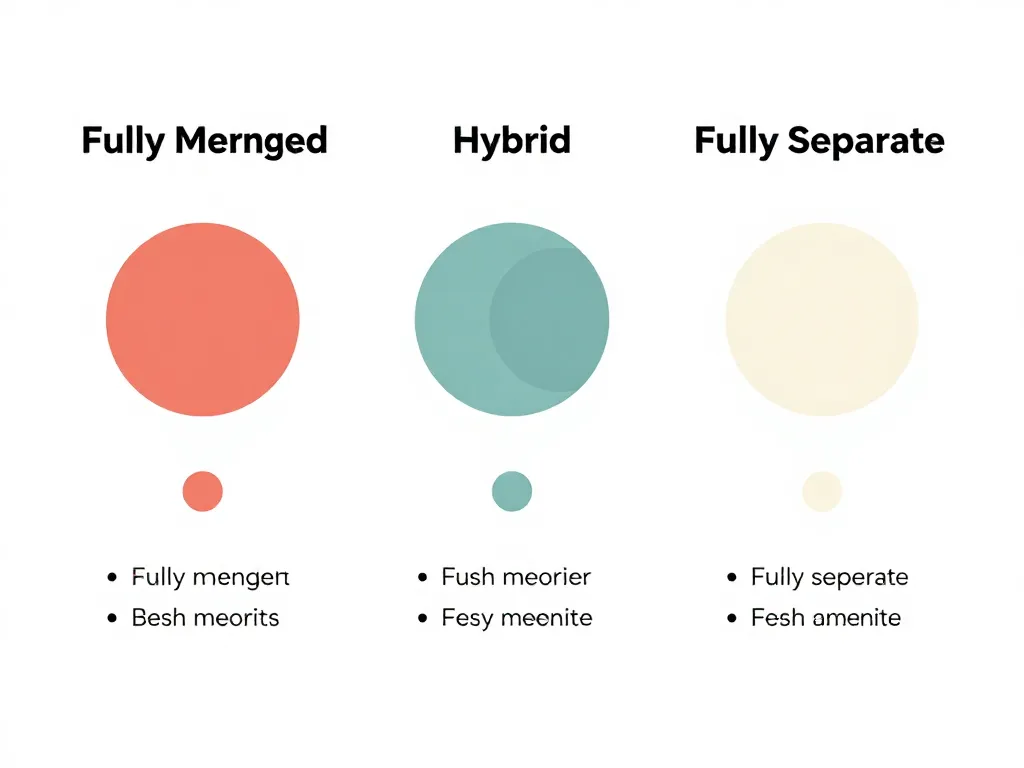

2. Choose Your Account Structure

There are three common models. None is inherently better.

Fully merged: All income goes into one joint account. All bills, savings, and spending come from it. - Best for: Couples who have similar spending habits, comparable incomes, and high mutual trust around money - Watch out for: Resentment if one partner feels monitored; power imbalance if one earns significantly more

Fully separate: Each partner keeps their own accounts. You split shared expenses by amount or percentage. - Best for: Couples with very different financial situations, second marriages, or strong independence needs - Watch out for: Feeling like roommates; logistical friction when splitting irregular expenses

Hybrid (yours, mine, ours): Each partner keeps a personal account with an agreed amount. The rest goes into a joint account for shared expenses and goals. - Best for: Most newlyweds, because it balances autonomy with partnership - Watch out for: The "agreed amount" needs to actually feel fair to both people

A note on the hybrid model: The most common version is to contribute proportionally to the joint account based on income. If one partner earns 60% of the household income, they contribute 60% to shared expenses. This tends to feel more equitable than a 50/50 split when there's an income gap.

3. Define "Shared" and "Personal" Expenses

This is where arguments live. Most couples agree that rent and utilities are shared. But what about:

- A gym membership only one person uses?

- Gifts for one partner's family?

- A hobby that costs $150 a month?

- Therapy for one partner?

- Student loan payments one partner brought into the marriage?

There are no universal right answers here. What matters is that you make explicit decisions instead of assuming you agree.

Try this: Each of you, independently, categorize the following as "shared" or "personal" — then compare your lists:

- Groceries

- Dining out together

- Dining out separately with friends

- Car insurance (for each car)

- Clothing

- Medical expenses

- Subscriptions (streaming, apps, etc.)

- Pet expenses

- Travel

- Gifts for each other's families

Wherever your lists differ, you've found a conversation worth having before it becomes a conflict.

4. Set a "Check-In Before Spending" Threshold

This is one of the simplest tools in the newlywed financial playbook, and one of the most effective. Agree on a dollar amount — say, $150 — above which either partner will mention the purchase to the other before buying.

This isn't about asking permission. It's about maintaining transparency. The number should be high enough that daily life isn't interrupted and low enough that neither person is blindsided.

Adjust over time. If $150 feels too restrictive after six months, raise it. If unexpected purchases keep creating tension, lower it.

5. Build a Financial Calendar

Don't rely on willpower or "we should talk about money more." Put structure in place.

- Weekly (5 minutes): Quick check-in. Any upcoming expenses? Anything unusual hit the account?

- Monthly (30 minutes): Review spending against your plan. Are you on track for savings goals? Any adjustments needed?

- Quarterly (1 hour): Bigger-picture review. Are your goals still aligned? Any life changes ahead (job change, baby, move) that require financial shifts?

- Annually (half-day): Full financial review. Update your shared document. Revisit your account structure. Celebrate progress.

Put these on a shared calendar. Treat them like doctor's appointments — non-negotiable, not optional.

6. Decide How to Handle Debt Together

If either partner brings debt into the marriage, you need a clear, spoken agreement about how to handle it. Options include:

- "Your debt, your responsibility": The partner who brought the debt pays it from personal funds. The other partner is not expected to contribute.

- "Our marriage, our debt": All debt becomes shared and is paid from joint funds.

- Hybrid approach: Joint funds cover minimum payments; the indebted partner directs extra personal funds toward accelerated payoff.

Whatever you choose, write it down. Not because you don't trust each other, but because memory is unreliable and resentment builds in the gaps between what two people remember agreeing to. Tools like Servanda can help couples formalize these kinds of financial agreements clearly, so there's no ambiguity when emotions get involved later.

7. Protect Each Other (Not Just Emotionally)

Newlywed financial planning isn't just about spending and saving. It's also about protection.

- Update beneficiaries on retirement accounts, life insurance, and investment accounts

- Review health insurance — does it make sense for one partner to cover both?

- Create or update wills and powers of attorney

- Decide on life insurance if either partner would struggle financially without the other's income

- Discuss disability insurance, especially if one partner is the primary earner

These aren't romantic topics. They are acts of care.

8. Plan for the Uneven Seasons

Most newlywed financial guides assume both partners are working full-time, with predictable income, indefinitely. Real life doesn't work that way. Someone may:

- Go back to school

- Take parental leave

- Lose a job

- Start a business

- Become a caregiver for a parent

Talk now about how you'd adjust your financial arrangement during these transitions. The couple who has a plan for a single-income season before it arrives handles it with far less stress than the couple who has to negotiate from inside the crisis.

Example: Marcus and David agreed before their wedding that if either partner wanted to pursue a career change, the other would cover shared expenses fully for up to twelve months — as long as the transition was discussed and planned in advance. When Marcus left his corporate job two years later to start a nonprofit, there was no argument. The agreement was already in place.

Common Mistakes Newlyweds Make With Money

A few patterns worth avoiding:

- Assuming your partner thinks about money the way you do. They don't. They grew up in a different house.

- Avoiding the topic until there's a problem. By the time you're arguing, positions are already hardened.

- Treating a financial disagreement as a character flaw. Your partner isn't "irresponsible" or "controlling" — they have a different relationship with money than you do.

- Setting a budget and never revisiting it. Your financial life will change. Your plan should change with it.

- Keeping financial secrets. Hidden accounts, unreported debts, and secret purchases erode trust faster than almost any other behavior in a marriage.

What If You're Already Arguing About Money?

If financial tension has already settled into your relationship, this checklist still works — but you may need to start with repair before you start with planning.

Acknowledge the tension directly: "I know money has been a sore spot for us. I want to fix that, and I think we need a plan — not just a conversation."

Then work through this checklist together, one item at a time, over several weeks. Don't try to resolve everything at once. Small agreements, kept consistently, rebuild trust faster than one big dramatic overhaul.

Conclusion

The question isn't really whether you should merge finances. It's how you want to handle money as a team — and that answer will be unique to your marriage. What matters is that the decision is made together, spoken aloud, written down, and revisited regularly.

Your financial arrangement doesn't need to look like anyone else's. It needs to work for the two of you — this year, and next year, and in the years that don't go according to plan.

Start with one item on this checklist today. The couple that builds a financial structure together doesn't eliminate disagreements — but they do stop being surprised by them. And that changes everything.

Frequently Asked Questions

Should newlyweds combine bank accounts or keep them separate?

There's no single right answer — it depends on your incomes, spending habits, and comfort levels. Most financial experts and newlyweds find a hybrid model (one joint account for shared expenses plus individual accounts for personal spending) strikes the best balance between teamwork and autonomy.

How do married couples handle debt one partner brought into the marriage?

Couples typically choose one of three approaches: the partner who brought the debt pays it alone, all debt becomes shared, or a hybrid where joint funds cover minimums while the indebted partner accelerates payoff from personal funds. The key is to discuss it explicitly and write down your agreement so there's no ambiguity later.

How often should married couples talk about finances?

Aim for a quick five-minute check-in weekly, a 30-minute budget review monthly, a one-hour goals review quarterly, and a comprehensive half-day financial review annually. Putting these on a shared calendar makes them routine rather than something triggered only by conflict.

What is a good spending limit before checking with your spouse?

Many couples start with a threshold between $100 and $200 — an amount high enough that daily purchases aren't interrupted but low enough to prevent surprises. Revisit and adjust this number every few months based on what's actually causing tension or feeling too restrictive.

How do you stop fighting about money as newlyweds?

Start by acknowledging the tension openly and then work through a structured financial checklist together over several weeks rather than in one overwhelming session. Small, clearly defined agreements that are consistently honored rebuild trust far more effectively than one dramatic financial overhaul.