Why Money Fights Destroy Marriages (And How to Stop)

It's 9:47 PM on a Tuesday. You're loading the dishwasher when you notice a shipping notification on your partner's phone — a $280 charge from a store you don't recognize. Your chest tightens. You weren't consulted. You think about the car payment due Friday, the credit card balance you've been chipping away at for two years, and the vacation fund that never seems to grow. By the time your partner walks into the kitchen, the question comes out sharper than you intended: "What's this charge?"

What follows isn't really about $280. It's about trust, control, values, fear, and the life you thought you were building together.

Money fights destroy marriages not because couples can't do math, but because money is never just about money. Research from Kansas State University found that financial disagreements are the single strongest predictor of divorce — stronger than arguments about children, in-laws, or intimacy. And yet most couples enter marriage without ever having a structured, honest conversation about their financial lives.

This article breaks down why that happens and, more importantly, what you can do about it starting tonight.

Key Takeaways

- Before creating a budget together, each partner should separately reflect on their "money story" — the childhood experiences and fears that shape how they view spending and saving — then share those stories with each other to build empathy.

- Set up a financial architecture with three components: a shared account funded by proportional income contributions, individual discretionary accounts with no-questions-asked spending, and named savings goals that create shared motivation.

- Schedule a consistent monthly money meeting with a structured agenda — celebrate a win, review numbers without blame, flag upcoming expenses, discuss one big-picture topic, and assign action items.

- Agree on a specific spending threshold (e.g., $100 or $500) above which both partners notify each other before purchasing, and put that agreement in writing so it's clear and revisitable.

- When money fights do happen, identify the emotional trigger beneath the surface topic and use recurring conflicts as signals that your financial system has a gap that needs closing.

The Real Reason Money Fights Are So Destructive

Money Is a Proxy for Everything Else

When couples argue about a credit card bill, they're rarely arguing about the number on the statement. They're arguing about what that number represents.

Financial psychologists call this your money story — a deeply ingrained set of beliefs about what money means, shaped by how you grew up. Consider these two people:

- Person A grew up in a household where money was tight. Saving feels like survival. Spending on anything non-essential triggers genuine anxiety.

- Person B grew up watching their parents work constantly but never enjoy their earnings. Spending feels like living. Hoarding money feels like wasting your life.

Neither person is wrong. But when they share a bank account, every transaction becomes a referendum on the other person's worldview. Person A sees Person B's purchase as reckless. Person B sees Person A's frugality as punishing. Both feel judged. Both dig in.

This is why money fights escalate faster than other disagreements. You're not debating a purchase — you're defending your identity.

Financial Conflict Triggers the Brain's Threat Response

Neuroscience research shows that financial stress activates the same brain regions as physical threat. When your partner makes a financial decision that feels unsafe, your amygdala fires as though you're in danger. You enter fight-or-flight mode, and suddenly you're not problem-solving anymore — you're surviving.

This explains why money arguments tend to be louder, longer, and more hurtful than other disputes. Your nervous system is treating a conversation about groceries like a conversation about whether you'll be okay.

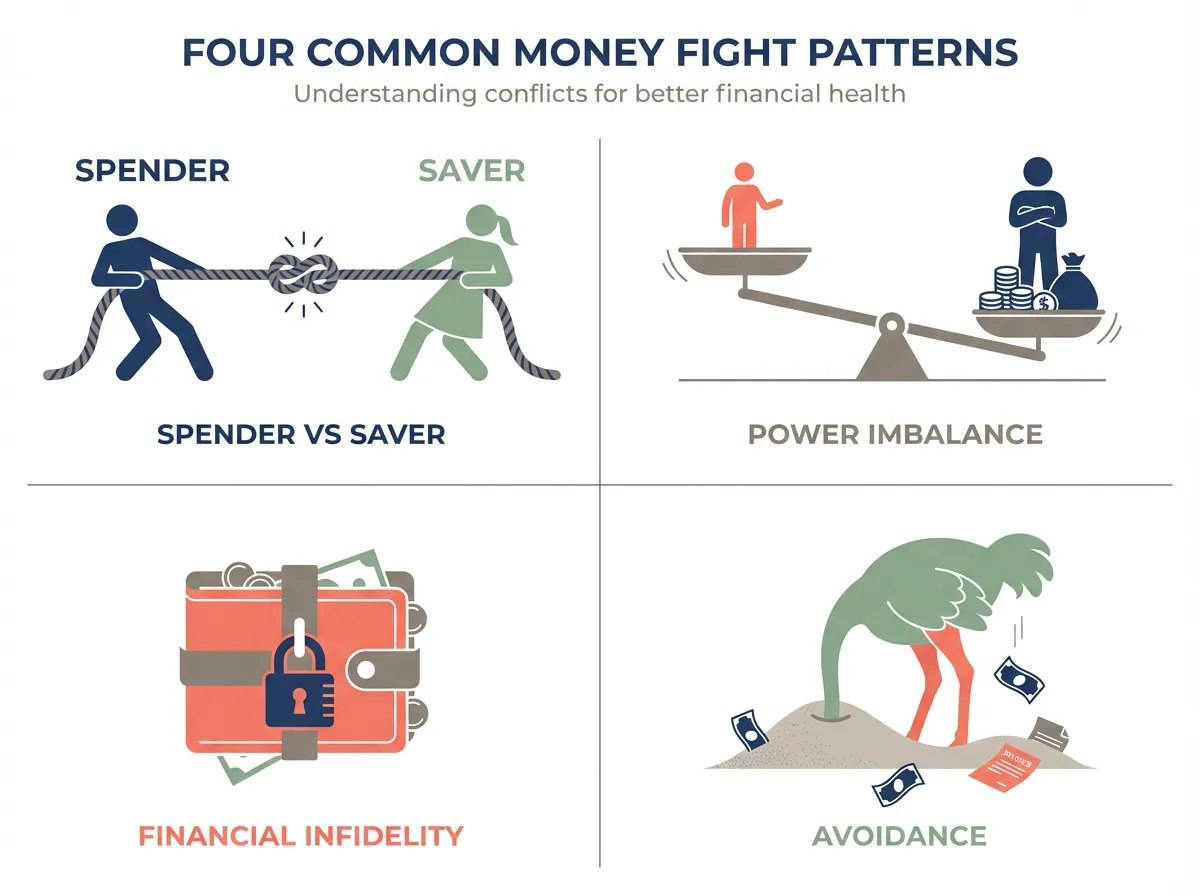

The Four Money Fight Patterns That Erode Marriages

Not all financial conflict looks the same. Recognizing your pattern is the first step toward breaking it.

1. The Spender vs. Saver Standoff

This is the most common dynamic: one partner tends toward spending, the other toward saving, and over time, each pushes the other further toward their extreme. The saver becomes more controlling. The spender becomes more secretive. Resentment compounds like interest.

What it sounds like: - "You never let us enjoy anything." - "You have no idea how close we are to the edge."

2. The Power Imbalance

When one partner earns significantly more — or when one partner stays home — money can become tangled with power. The higher earner may feel entitled to more say. The lower earner may feel they need permission to spend. Neither person may say this out loud, but the dynamic poisons daily interactions.

3. Financial Infidelity

Secret accounts. Hidden purchases. Undisclosed debts. A 2023 Bankrate survey found that 39% of partnered adults admit to financial deception. Financial infidelity shatters trust in the same way other forms of betrayal do — and in some ways it's harder to recover from, because the evidence is concrete and ongoing.

4. Avoidance

Some couples never fight about money — because they never talk about it at all. They split things informally, avoid looking at statements together, and treat the subject as too uncomfortable to raise. This isn't peace. It's a slow-building crisis.

How to Stop Money Fights Before They Start

The goal isn't to eliminate all financial disagreement — that's neither realistic nor healthy. The goal is to build a shared system that makes conflict productive instead of corrosive. Here's how.

Step 1: Surface Your Money Stories (Before Building a Budget)

Before you open a spreadsheet, sit down and have a conversation that most couples skip entirely. Each person answers these questions — separately first, then together:

- What did money mean in your childhood home? Was it scarce? Abundant? A source of tension? A taboo topic?

- What's your biggest financial fear? Not having enough? Missing out on life? Being controlled? Being judged?

- What does financial security look like to you? A specific number in savings? Owning a home outright? Being able to quit a bad job?

- What purchase or financial decision makes you happiest? Travel? Giving to others? Investing? A well-stocked fridge?

The point isn't to agree. It's to understand. Once you see that your partner's spending habits come from the same emotional logic as your saving habits — a need to feel safe and valued — the judgment softens.

Step 2: Create a Joint Financial Architecture (Not Just a Budget)

A budget is a document. A financial architecture is a system that accounts for both partners' psychological needs. Here's a structure that works for many couples:

- Shared account for shared expenses. Mortgage, utilities, groceries, childcare, insurance. Both partners contribute a proportional percentage of their income (not a flat amount — more on this below).

- Individual discretionary accounts. Each partner gets an agreed-upon amount per month that is theirs to spend with zero justification required. This eliminates the "permission" dynamic and respects autonomy.

- Shared savings categories with named goals. "Emergency fund" is too vague to motivate anyone. Name the goals: "Six-month safety net," "Japan trip 2026," "Kitchen renovation." Named goals create shared excitement instead of shared deprivation.

Why proportional contributions matter: If one partner earns $90,000 and the other earns $50,000, a 50/50 split creates resentment. Proportional contribution (each putting in, say, 60% of their income toward shared expenses) keeps the financial weight balanced relative to capacity. This is especially critical in couples where one partner has chosen lower-paying work to support the family in other ways.

Step 3: Schedule a Monthly Money Meeting (And Make It Bearable)

The couples who handle money well aren't the ones who never disagree — they're the ones who have a recurring, low-stakes space to talk about it.

Here's a format that prevents these meetings from becoming arguments:

- Celebrate a win (2 minutes). Start with something that went right. A bill paid off. A savings milestone hit. A spending decision you're proud of.

- Review the numbers (10 minutes). Look at actual spending vs. your plan. No blame. Just data.

- Flag upcoming expenses (5 minutes). Car registration, birthday gifts, holiday travel. Surprises are the enemy.

- Discuss one bigger-picture item (10 minutes). This is where you talk about the raise, the new job possibility, the aging parent, the college fund. One topic per meeting. Don't try to solve everything.

- Agree on action items (3 minutes). Who does what before the next meeting?

Some couples do this over coffee on a Sunday morning. Others make it a Friday night ritual with takeout. The medium doesn't matter. The consistency does.

Step 4: Establish Spending Thresholds — In Writing

One of the simplest interventions is agreeing on a spending threshold: an amount above which both partners check in before purchasing. It might be $100. It might be $500. The number depends on your income and comfort level.

The critical piece: this goes both ways, and it's about notification, not permission. The conversation is, "Hey, I'm looking at this $350 jacket — here's why I want it," not, "May I please buy a jacket?"

Putting these agreements in writing — even informally — makes them stick. Tools like Servanda can help couples formalize shared financial agreements so that expectations are clear and revisitable, rather than relying on memory or assumed understanding.

Step 5: Address Debt as a Team (Even When It's "Your" Debt)

Few topics generate more resentment than pre-existing debt. One partner may have entered the relationship with student loans, credit card balances, or medical debt. The other may feel it's unfair to share that burden.

Here's the reframe: once you've committed to a shared life, your partner's debt affects your shared future. That doesn't mean you split it 50/50 — it means you have an honest strategy for addressing it that both people feel is fair.

Options couples use:

- The proportional approach: Both partners contribute to debt payoff relative to their incomes.

- The timeline approach: The partner with debt commits to a payoff timeline; the other partner supports by covering more shared expenses during that period.

- The hybrid approach: Shared minimum payments from the joint account; extra payments come from the debtor's discretionary fund.

What matters is that the plan exists, that both people agreed to it, and that it's revisited regularly.

Step 6: Know When You Need a Third Party

If your money fights consistently escalate into personal attacks, if there's active financial infidelity, or if one partner shuts down completely when finances come up, a couples therapist who specializes in financial conflict can make an enormous difference.

This isn't a failure. It's a recognition that the emotional wiring around money runs deep — often deeper than two people can untangle on their own. A skilled therapist helps you see the fear beneath the frustration and build responses that don't cause harm.

What to Do After a Money Fight

Even with the best systems, money arguments will happen. What distinguishes resilient couples from struggling ones is what happens in the aftermath.

- Don't pretend it didn't happen. Unresolved financial conflict doesn't dissolve — it accumulates.

- Identify the trigger, not just the topic. "We fought about the electric bill" is the surface. "I felt scared because we're behind on savings" is the truth.

- Separate the financial decision from the relationship question. The question isn't "Should we have bought that?" It's "How do we make these decisions together so we both feel respected?"

- Revisit your system. If fights keep recurring around the same issue, that's information. Your financial architecture has a gap. Close it.

Conclusion

Money fights destroy marriages not because couples are bad with money, but because money carries the full weight of our deepest fears and values — and most couples never learn how to talk about it that way. The research is clear: it's not how much you earn that predicts marital satisfaction. It's whether you have a shared, transparent system for managing what you have.

You don't need to agree on every purchase. You don't need identical money stories. You need a structure that honors both partners' needs, a recurring space to adjust it, and the willingness to see your partner's financial behavior as information about their inner world — not an attack on yours.

The $280 charge on a Tuesday night doesn't have to end in a fight. It can end in a conversation. And that conversation can make your marriage stronger than it was the day before.

Frequently Asked Questions

Why do couples fight about money more than anything else?

Money arguments are so destructive because money is a proxy for deeper issues like trust, control, security, and personal values. Research from Kansas State University found that financial disagreements are the single strongest predictor of divorce, largely because they activate the brain's threat response and make partners feel like their identity and safety are under attack.

How do you talk to your spouse about money without starting a fight?

Start by understanding each other's "money stories" — the childhood experiences that shaped your financial beliefs — so you can approach conversations with empathy rather than judgment. Then establish a regular, low-stakes monthly money meeting with a structured agenda that begins with celebrating a win and focuses on data rather than blame.

Should married couples split expenses 50/50 or by income?

Most financial therapists recommend proportional contributions based on each partner's income rather than a flat 50/50 split. When one partner earns significantly more, an equal split can breed resentment, while proportional sharing keeps the financial burden balanced relative to each person's capacity and acknowledges non-monetary contributions to the household.

What is financial infidelity and how common is it?

Financial infidelity includes secret accounts, hidden purchases, and undisclosed debts — and a 2023 Bankrate survey found that 39% of partnered adults admit to some form of financial deception. It shatters trust in a way similar to other forms of betrayal and can be especially hard to recover from because the evidence is concrete and often ongoing.

When should couples see a therapist for money problems?

Seek a couples therapist who specializes in financial conflict if your money fights consistently escalate into personal attacks, if there's active financial infidelity, or if one partner completely shuts down whenever finances come up. Professional help isn't a sign of failure — it's a recognition that the emotional wiring around money often runs deeper than two people can untangle on their own.