Why You Keep Fighting About Money (And How to Stop)

It's Tuesday night, and the credit card statement just arrived. One of you sees a $200 charge at a sporting goods store. The other sees a $140 charge at a restaurant from last weekend's dinner with friends. Within minutes, you're not just talking about the charges — you're relitigating every financial decision of the past six months. He says she's "reckless." She says he's "controlling." You both go to bed angry, knowing this same fight will surface again next month under a slightly different disguise.

If this sounds familiar, you're far from alone. Research consistently shows that fighting about money is one of the top predictors of divorce, outranking disagreements about chores, in-laws, and even intimacy. But here's what most advice gets wrong: the problem isn't your budget. It's that you and your partner are operating from two completely different financial blueprints — invisible scripts about money written long before you ever met.

This article will show you exactly where those scripts come from and give you a practical framework to rewrite them together.

Key Takeaways

- Your money fights aren't really about money. They're about conflicting values, fears, and beliefs shaped by your childhood experiences with finances.

- Each partner carries a "financial blueprint" — an unconscious set of rules about earning, saving, and spending — that often directly conflicts with their partner's.

- Budgeting alone won't fix the problem. You need to align on why money matters to each of you before you can agree on how to manage it.

- A "Money Story" conversation — where each partner shares the financial experiences that shaped them — can defuse years of tension in a single evening.

- Written financial agreements on specific triggers (dining out, gifts, personal spending) prevent the same fights from recurring month after month.

The Real Reason Couples Keep Fighting About Money

Let's be honest: if the problem were just math, you'd have solved it already. You're both intelligent adults. You can read a spreadsheet. The reason money fights keep cycling back isn't a lack of information — it's a clash of meaning.

When one partner says, "We can't afford that," they might actually be saying, "Spending that amount makes me feel unsafe." When the other partner says, "You never let us enjoy our money," they might actually be saying, "I feel controlled, the same way I felt growing up."

Money is never just money. It's a proxy for security, freedom, power, love, and identity. And until you understand what money means to each of you, no budgeting app or envelope system will stop the arguments.

What Is a Financial Blueprint?

A financial blueprint is the set of unconscious beliefs, emotional associations, and behavioral patterns around money that you developed in childhood and early adulthood. Think of it as your internal operating system for financial decisions.

Your blueprint was shaped by:

- What you observed: Did your parents fight about money openly or treat it as taboo? Did one parent control the finances while the other was kept in the dark?

- What you experienced: Did you grow up with scarcity — stretching meals, hand-me-down clothes, utilities getting shut off? Or did you grow up with abundance and the anxiety of maintaining it?

- What you were told: "Money doesn't grow on trees." "Rich people are greedy." "Always save for a rainy day." "You deserve the best." These phrases embed themselves deep.

- What you felt: Was money a source of stress, shame, pride, or power in your household?

These experiences create deeply held financial identities. Researchers and financial therapists often categorize people into money archetypes.

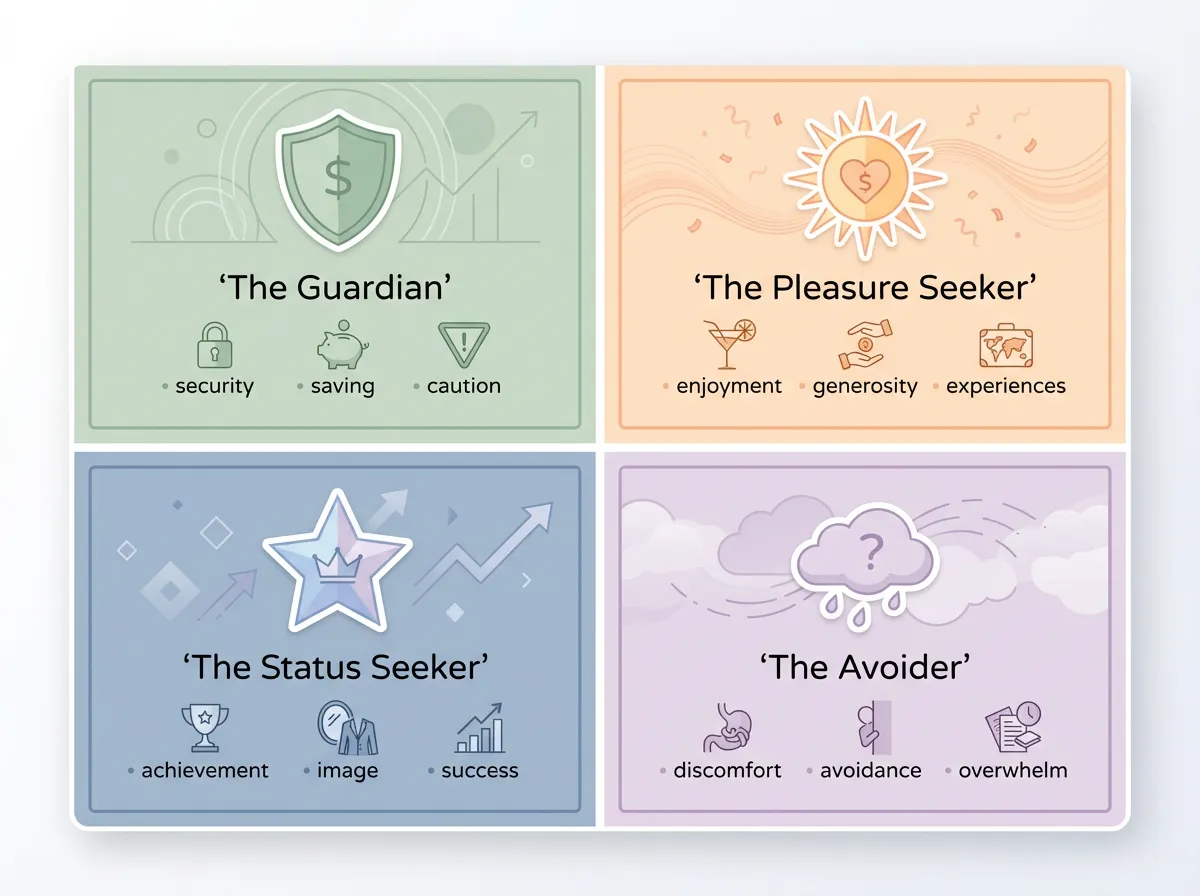

The Four Money Archetypes

- The Guardian — Prioritizes security and saving. May come across as restrictive. Often grew up in environments where money was scarce or unpredictable.

- The Pleasure Seeker — Values enjoyment and generosity. May come across as impulsive. Often grew up either in deprivation (and vowed to never feel that way again) or in households where spending equaled love.

- The Status Seeker — Associates money with achievement and image. May overspend to project success. Often grew up in environments where worth was measured by visible wealth.

- The Avoider — Dislikes thinking about money altogether. May ignore bills or refuse to engage in financial planning. Often grew up in homes where money caused pain or conflict.

No archetype is right or wrong. But when a Guardian partners with a Pleasure Seeker — which happens frequently, because opposites genuinely attract — the stage is set for recurring conflict.

Why Traditional Budgeting Advice Fails Couples

Most financial advice for couples jumps straight to tactics: "Use the 50/30/20 rule." "Automate your savings." "Set a spending limit and stick to it."

This advice isn't wrong, but it's incomplete. It's like telling two people who disagree about where to drive to just agree on a speed limit. The destination matters more than the speedometer.

Here's what typically happens:

- A couple fights about money.

- They sit down and create a budget.

- The budget reflects one partner's values more than the other's (usually whoever is more financially dominant or assertive).

- The other partner feels constrained, resentful, or unheard.

- They "cheat" the budget or passively resist it.

- The fight resurfaces — now with an added layer of broken trust.

Sound familiar? That's because the budget was treating a symptom, not the cause.

The Money Story Conversation: A Framework That Actually Works

Instead of starting with a spreadsheet, start with a story. The Money Story Conversation is a structured exercise where each partner shares their financial history — not their current account balances, but the emotional narrative of how they learned about money.

How to Have the Conversation

Set the stage: - Choose a calm, private moment — not during or after a fight - Agree that this isn't a debate; it's a listening exercise - Each person gets uninterrupted time to share (15-20 minutes each)

Each partner answers these prompts:

- What is your earliest memory involving money?

- How did your parents or caregivers handle money? Did they fight about it? Avoid it? Control it?

- What phrases about money did you hear growing up?

- When you think about not having enough money, what specifically scares you? What's the worst-case scenario in your mind?

- When you think about having plenty of money, what does that life look like? What does it feel like?

- What does money represent to you in one word? (Security? Freedom? Success? Peace? Fun?)

After both partners have shared: - Reflect back what you heard without judgment: "It sounds like money means safety to you because growing up, it felt like things could fall apart at any time." - Identify where your blueprints align and where they diverge - Acknowledge that neither blueprint is wrong — they're just different

A Real Example

Consider a couple we'll call Marcus and Leah. Marcus grew up in a household where his father was laid off twice. He remembers his mother crying at the kitchen table over bills. For Marcus, money means security, and his blueprint says: save aggressively, spend minimally, always prepare for the worst.

Leah grew up in a household that was financially stable but emotionally cold. The only time her parents seemed happy was on family vacations or when buying gifts. For Leah, money means connection, and her blueprint says: spending on experiences and people is how you show love.

When Leah books a weekend getaway, Marcus feels anxiety. When Marcus questions the expense, Leah feels rejected. Neither is being irrational — they're both acting from deeply ingrained blueprints.

Once they understood each other's Money Stories, the fights changed. Marcus could say, "I know this trip is important to you — my anxiety isn't about the trip, it's about the number in our savings account dropping below what feels safe to me." And Leah could say, "I hear that. Can we find a trip budget that lets me plan something meaningful without crossing your safety threshold?"

That's not a budget conversation. That's a values conversation. And it's the only kind that sticks.

From Values to Agreements: Making It Concrete

Once you understand each other's financial blueprints, you can build agreements that honor both. Here's a practical process:

Step 1: Define Your Shared Financial Values

Write down 3-5 values you both agree on. For example: - "We value financial security — we always want at least 3 months of expenses saved." - "We value shared experiences — we'll prioritize a travel fund." - "We value personal autonomy — each of us gets discretionary spending, no questions asked."

Step 2: Identify Your Top 3 Triggers

Be specific. Instead of "spending too much," try: - "Purchases over $150 that aren't discussed first" - "Lending money to family members without agreement" - "Putting non-essential items on credit cards"

Step 3: Create Specific, Written Agreements

For each trigger, agree on a clear protocol: - "Any individual purchase over $100 gets a quick text to the other person — not for permission, but as a heads-up." - "We each get $200/month of personal spending that doesn't require discussion or justification." - "Family financial requests over $500 are discussed together before we respond."

Writing these down matters. Spoken agreements are easily forgotten or remembered differently by each partner. Tools like Servanda can help couples formalize these financial agreements in writing, making it easier to revisit and adjust them as circumstances change — without relying on memory or restarting the same argument.

Step 4: Schedule a Monthly Money Check-In

Not a fight. Not an audit. A 30-minute, judgment-free review: - Are we on track with our shared values? - Did anything trigger one of us this month? - Do any of our agreements need adjusting?

Treat it like a team meeting, not a tribunal. Some couples pour a glass of wine, order takeout, or hold the check-in at a coffee shop to keep the tone relaxed.

What to Do When You're Mid-Fight Right Now

Sometimes you need a framework for the long term and a lifeline for tonight. If you're in the middle of a money fight, try these three steps:

- Pause and name the blueprint. Say, "I think my savings anxiety is talking right now," or "I realize I'm feeling controlled, and that's triggering something old for me." Naming it takes the charge out of it.

- Separate the decision from the emotion. Agree to table the specific financial decision for 48 hours. Most money decisions aren't truly urgent.

- Ask the clarifying question. Instead of "Why did you spend that?" ask, "What did that purchase mean to you?" The answer will surprise you — and it will move the conversation forward instead of in circles.

Frequently Asked Questions

Is it normal for couples to fight about money?

Absolutely. Studies consistently rank money as one of the top sources of conflict for couples at every income level. It's not about how much you have — it's about differing values and expectations. The goal isn't to never disagree, but to understand each other well enough that disagreements become productive conversations instead of recurring fights.

How do you talk to your partner about money without starting a fight?

Timing and framing matter enormously. Don't bring up money during a stressful moment or in response to a specific purchase. Instead, schedule a dedicated time, lead with curiosity rather than accusations, and start by sharing your own financial fears and values before asking about theirs. The Money Story Conversation framework above is specifically designed for this.

Should couples combine finances or keep them separate?

There's no universally right answer — it depends on your shared values, individual comfort levels, and practical circumstances. Many couples find a hybrid approach works best: a joint account for shared expenses and goals, plus individual accounts for personal discretionary spending. The key is that the system you choose reflects values you've both explicitly agreed on, rather than defaulting to one partner's preference.

What if my partner refuses to talk about money at all?

Avoidance around money is often rooted in shame, anxiety, or past trauma — not laziness or disrespect. If your partner shuts down during money conversations, try lowering the stakes: share your own Money Story first without asking them to reciprocate. Often, vulnerability is contagious. If avoidance persists and is causing real harm to the relationship, a financial therapist can provide a safe, structured environment to begin the conversation.

Can money problems actually end a relationship?

They can — but it's rarely the money itself that ends things. It's the erosion of trust, the feeling of being unheard, and the resentment that builds from years of unresolved conflict. The couples who navigate money differences successfully aren't the ones who agree on every purchase — they're the ones who've built a shared understanding of what money means to each of them and created agreements that honor both perspectives.

Moving Forward Together

If you've been fighting about money for months or years, it can feel like the problem is intractable — just a fundamental incompatibility you have to live with. It's not.

The truth is that most money fights are solvable once you stop treating them as financial problems and start treating them as emotional ones. Your partner isn't the enemy. Their financial blueprint is just different from yours, shaped by a childhood you didn't share.

Start with the Money Story Conversation. Listen without defending. Then build agreements that reflect both of your values — not just one person's spreadsheet. The couples who thrive financially aren't the ones who never disagree. They're the ones who've learned to disagree with understanding, make decisions with intention, and revisit those decisions with grace.

You didn't choose your financial blueprint. But you can choose, together, to write a new one.