Money Fights in Relationships: A Couples Guide

It's a Tuesday night. One partner opens the credit card statement and sees a $280 charge at a home goods store. The other partner doesn't see the problem — it was a "good deal" on things the house needed. Within minutes, the conversation spirals. It's not really about throw pillows or a new lamp anymore. It's about safety, control, respect, and two very different ideas about what money means.

If this sounds familiar, you're far from alone. Financial disagreements are consistently ranked among the top predictors of divorce, and research from Kansas State University found they're the strongest type of argument for forecasting relationship breakdown — more than fights about chores, in-laws, or even intimacy. Yet most advice tells couples to "just make a budget together," as if the real problem is arithmetic.

It isn't. Money fights in relationships almost always run deeper than dollars and cents. This guide will help you understand why you and your partner clash over finances and give you practical tools to change the pattern for good.

Key Takeaways

- Money conflicts are identity conflicts. Your spending and saving habits were shaped by your family long before you met your partner. Recognizing this transforms blame into curiosity.

- The "presenting issue" is rarely the real issue. A fight about a $50 purchase is usually a fight about values, security, or autonomy.

- Budgets fail without shared meaning. Spreadsheets only work after you've aligned on what money represents to each of you.

- Regular, low-stakes money conversations prevent high-stakes blowups. Scheduled financial check-ins reduce the emotional charge around money topics.

- Written agreements create safety. Putting financial boundaries and shared decisions in writing reduces ambiguity and resentment.

Why Couples Really Fight About Money

On the surface, money fights in relationships look straightforward: one person spends too much, or the other saves too aggressively, or someone hid a purchase. But beneath nearly every financial disagreement is a collision of money stories — the unconscious beliefs about money each partner absorbed growing up.

Your Family's Money Script

Financial psychologist Dr. Brad Klontz coined the term "money scripts" to describe the beliefs about money that form in childhood and operate largely outside awareness. These scripts fall into broad patterns:

- Money avoidance: "Rich people are greedy. It's virtuous not to care about money." (Common in families where money was associated with conflict or moral failure.)

- Money worship: "More money will solve everything. I'll be happy when I earn enough." (Common in families that experienced financial instability.)

- Money status: "Your net worth equals your self-worth." (Common in families where success was measured externally.)

- Money vigilance: "You should always save. Spending is risky." (Common in families that survived economic hardship through extreme discipline.)

Now imagine a partner raised with money vigilance falling in love with a partner raised with money avoidance. One tracks every dollar and feels anxious when the savings account dips. The other finds the tracking suffocating and feels judged for every purchase. Neither is wrong. They're operating from two different emotional operating systems.

The Identity Layer You're Missing

Here's what budgeting apps can't tell you: when your partner criticizes your spending, it can feel like they're criticizing who you are and where you come from. If your mother showed love by being generous with gifts, and your partner calls that "wasteful," it doesn't just sting — it feels like an attack on your family, your values, your entire upbringing.

This is why money fights escalate so quickly and feel so personal. You're not arguing about the electric bill. You're defending your identity.

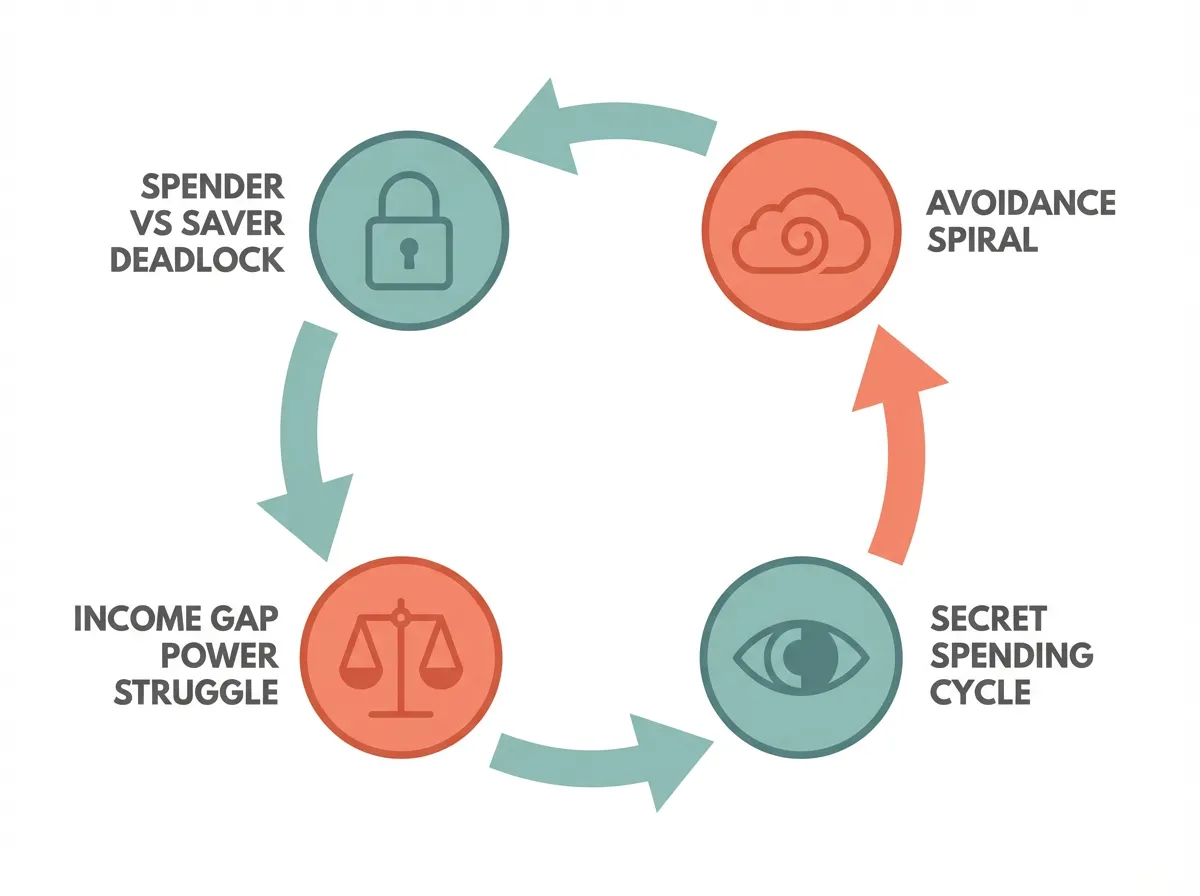

The Four Patterns That Keep Money Fights Recurring

If you and your partner have the same financial argument on a loop, you're likely stuck in one of these patterns:

1. The Spender vs. Saver Deadlock

This is the most common dynamic. One partner feels controlled; the other feels unsafe. The saver tightens the budget; the spender rebels with a purchase; the saver reacts with frustration — and the cycle repeats.

What's really happening: The saver's need for security and the spender's need for autonomy are both legitimate. The conflict isn't about who's "right" — it's about two unmet needs colliding.

2. The Income Gap Power Struggle

When one partner earns significantly more, money can become tangled with power. The higher earner may feel entitled to more decision-making authority. The lower earner may feel they have to "ask permission" to spend, which breeds resentment.

What's really happening: The couple hasn't explicitly negotiated how income relates to ownership and decision-making. Without that conversation, assumptions fill the void — and assumptions breed conflict.

3. The Secret Spending / Financial Infidelity Cycle

One partner hides purchases, maintains secret accounts, or lies about debt. When discovered, trust collapses. The offending partner promises transparency, but the surveillance-and-secrecy dynamic often continues.

What's really happening: The person hiding spending usually feels they've lost all financial autonomy in the relationship. Secrecy feels like the only way to preserve a sense of self. This doesn't excuse it — but understanding the motive changes how you address it.

4. The Avoidance Spiral

Both partners sense that money is a dangerous topic, so they simply never discuss it. Bills get paid (or don't), debt accumulates quietly, and resentment builds until it explodes over something seemingly trivial.

What's really happening: Both partners have learned — probably from their families — that money conversations are inherently combative. So they avoid them, which guarantees the very explosion they fear.

How to Break the Cycle: A Step-by-Step Approach

You don't need to agree on every financial decision. You need a process that makes disagreement safe. Here's how to build one.

Step 1: Map Your Money Stories (Before Talking Numbers)

Before you open a single bank statement together, sit down and answer these questions individually, then share your answers:

- What did money mean in your family growing up? Was it abundant or scarce? A source of pride or shame? Freely discussed or completely taboo?

- What's your earliest memory involving money? (This often reveals a formative emotional experience.)

- What's the financial situation you fear most? Bankruptcy? Being controlled? Being seen as cheap? Being seen as irresponsible?

- What does financial "success" look like to you? A paid-off house? Freedom to travel? A fat retirement account? The ability to be generous?

The goal here isn't to solve anything. It's to understand. When you hear your partner describe growing up watching their parents fight every month about whether they could afford groceries, their obsessive budgeting suddenly makes sense — not as a personality flaw, but as a survival strategy.

Step 2: Name the Real Conflict Beneath the Money Fight

The next time a financial disagreement surfaces, pause and ask yourselves: "What is this fight actually about?"

Use this framework:

- Security: "I need to feel like we're safe and prepared for the worst."

- Freedom: "I need to feel like I have autonomy and choice."

- Fairness: "I need to feel like this partnership is equitable."

- Values: "I need to feel like our money reflects what matters to us."

- Trust: "I need to feel like we're being honest with each other."

Naming the deeper need transforms the conversation. "You spent too much at dinner" becomes "I'm feeling anxious about our security this month, and I need reassurance." That's a conversation you can actually work with.

Step 3: Create a Financial Structure You Both Designed

Once you understand each other's money stories and core needs, then you can talk about systems. The key: both partners must have input, and the structure must honor both people's needs.

Here's a framework many couples find effective:

- Shared account for joint expenses (housing, groceries, utilities, shared goals)

- Individual accounts for personal spending — no questions asked, no judgment, within an agreed-upon amount

- A "big purchase" threshold — any purchase above a certain dollar amount (say, $150) gets a conversation first

- A shared savings goal that you're both emotionally invested in

The individual accounts piece is especially important. It eliminates the surveillance dynamic that drives secret spending. Both partners get autonomy within a structure they co-created.

Step 4: Schedule Regular Money Check-Ins

The couples who fight least about money aren't the ones who agree on everything — they're the ones who talk about it regularly when they're not already upset.

A weekly or biweekly 20-minute "money meeting" can include:

- Reviewing upcoming expenses

- Checking progress on shared savings goals

- Flagging any purchases or expenses that feel stressful

- Adjusting the budget if something isn't working

Pro tip: Keep these meetings short, agenda-driven, and judgment-free. Some couples pour a glass of wine or make it part of a date night to reduce the clinical feel.

Step 5: Put Your Agreements in Writing

This step might feel overly formal between romantic partners, but it's one of the most powerful things you can do. When financial agreements live only in memory, each partner remembers them slightly differently — and that gap becomes its own source of conflict.

Write down:

- Your agreed-upon monthly budget

- The "big purchase" conversation threshold

- How individual spending accounts work

- Your shared financial goals and timelines

- What happens when one of you wants to change the plan

This isn't a legal contract. It's a shared document that gives you something concrete to return to when emotions get heated. Tools like Servanda can help couples formalize these kinds of agreements in writing so that the terms are clear and revisitable, rather than subject to the fog of a tense conversation.

When the Real Problem Isn't Money at All

Sometimes, persistent money fights are a proxy for a relationship issue that has nothing to do with finances:

- A power imbalance that shows up most visibly through financial control

- Unprocessed resentment from a past betrayal that gets channeled into financial criticism

- Fundamentally different visions for the future that neither partner wants to confront directly

If you've done the work above — mapped your money stories, named the deeper needs, created a fair structure — and the fights continue with the same intensity, consider whether the real issue lives somewhere else entirely. A couples therapist, particularly one trained in financial therapy, can help you untangle what money is masking.

A Real-World Example

"Priya" and "David" had been together for six years. Priya grew up in a family of immigrants who saved relentlessly and viewed any non-essential purchase as reckless. David grew up comfortably middle-class in a family that spent freely and equated generosity with love.

Their recurring fight: David would book a weekend trip or buy gifts for friends, and Priya would feel panicked. She'd criticize the spending; he'd feel controlled and ashamed. He started hiding small purchases. When she found out, trust eroded further.

What changed: They sat down and shared their money stories. Priya described her parents' fear of financial ruin and how saving was an act of love and survival in her family. David described how his parents used spending as a way to connect and create joy. For the first time, they saw each other's behavior as loving rather than threatening.

They created a system: shared expenses from a joint account, $300/month each in personal accounts (no questions asked), and a $200 purchase threshold for joint discussion. They also set a shared goal — a house down payment — that gave Priya's need for security a target and gave David's desire for a tangible, exciting future something to rally around.

The fights didn't vanish overnight. But they became shorter, less personal, and more productive. Most importantly, neither partner felt like the villain anymore.

Frequently Asked Questions

How do I bring up money with my partner without starting a fight?

Timing and framing matter enormously. Don't bring up money in the heat of the moment or immediately after a purchase. Instead, choose a calm time and lead with curiosity rather than accusation. Try: "I'd love for us to set aside 20 minutes this week to talk about our finances — not because anything is wrong, but because I want us to feel like a team about this."

Should couples combine all their finances or keep them separate?

There's no single right answer. Research suggests that some degree of both — a shared account for joint responsibilities and individual accounts for personal spending — tends to reduce conflict while maintaining both partnership and autonomy. The critical thing is that whatever system you choose, both partners have an equal voice in designing it.

What if my partner refuses to talk about money at all?

Avoidance usually stems from anxiety or shame, not indifference. Rather than pushing harder, try naming what you observe: "I notice we both get tense when money comes up. I wonder if we've both had experiences that make this topic feel unsafe." If avoidance persists and is causing real problems, a therapist who specializes in financial therapy can provide a structured, neutral environment for the conversation.

Is financial infidelity as serious as other forms of betrayal?

For many couples, yes. Hidden debt, secret accounts, or undisclosed spending can shatter trust just as deeply as other forms of dishonesty. The severity often depends on the scale and duration of the deception. The path forward is similar to recovering from other trust violations: full disclosure, understanding why the secrecy happened, and building new systems with transparency baked in.

At what point should we get professional help for money fights?

Consider professional help if your money arguments have become circular (same fight, no progress), if financial infidelity has occurred, if one partner is using money to control the other, or if money conflicts are damaging your emotional or physical intimacy. Financial therapists specifically are trained to address both the emotional and practical dimensions of financial conflict in relationships.

Moving Forward Together

Money fights in relationships are painful precisely because they're never just about money. They're about safety, identity, power, and the future you're trying to build together. The good news is that understanding this — truly absorbing that your partner's financial behavior comes from a place as deep and formative as your own — changes everything.

You don't need to have identical money personalities. You need to understand each other's money stories, name the real needs beneath the surface-level arguments, and build a financial system that gives both of you a genuine voice.

Start this week. Share one money memory from your childhood with your partner. Listen to theirs without judgment. That single conversation may do more for your finances — and your relationship — than any spreadsheet ever could.