Money Fights Are Ruining Your Relationship

It's 9:47 PM on a Tuesday. You're exhausted, scrolling through your bank app, and there it is — a $214 charge at a store you don't recognize. Your stomach drops. Not because the money is gone, but because you already know what happens next. The question. The defensive response. The escalation. Within ten minutes, you're no longer arguing about $214. You're arguing about who works harder, who sacrifices more, and whether your partner even respects you at all.

If this sounds familiar, you're far from alone. Studies consistently rank money as one of the top sources of conflict in romantic relationships, and with inflation squeezing household budgets tighter than ever, those fights are getting louder and more frequent. Money fights in relationships aren't really about money — they're about trust, values, security, and power. And until you address what's underneath the numbers, the fights will keep coming back.

This article is your roadmap to breaking that cycle.

Key Takeaways

- Money fights are rarely about the money itself. They're fueled by deeper fears around security, control, and feeling valued in the relationship.

- The "blame game" starts when couples skip alignment on values and jump straight to budgets. Talk about what money means to each of you before you talk about where it goes.

- Scheduled money conversations dramatically reduce surprise blowups. A 20-minute weekly "money date" can replace months of simmering resentment.

- You don't need to merge everything or agree on every purchase. A structure that gives both partners autonomy and shared accountability works better than forced uniformity.

- Financial stress from external pressures (inflation, job loss, debt) requires you to fight together against the problem, not against each other.

Why Money Fights in Relationships Cut So Deep

Most couples assume their money fights are about the specific transaction — the impulse purchase, the forgotten bill, the credit card balance. But research from Kansas State University found that arguments about money are the single strongest predictor of divorce, more than arguments about chores, sex, or in-laws. Why?

Because money is never just money. It's a proxy for nearly every emotional need in a relationship:

- Security: "If we can't pay rent, what happens to us?"

- Respect: "You spent that without even asking me?"

- Freedom: "I feel like I need permission to buy anything."

- Fairness: "I earn more, so why don't I get more say?"

- Trust: "You hid that debt from me for how long?"

When your partner questions a purchase, your brain doesn't process it as a neutral financial inquiry. It processes it as a threat to your autonomy, your judgment, or your worth. That's why a conversation about a grocery bill can spiral into a full-blown identity crisis in under sixty seconds.

The Inflation Factor

This dynamic has intensified dramatically in recent years. With the cost of groceries, housing, childcare, and insurance climbing faster than wages, couples who once had enough breathing room to absorb each other's spending habits are now operating with razor-thin margins. There's less room for error — and less patience when an error happens.

A 2023 survey by the American Psychological Association found that 65% of adults cite money as a significant source of stress. When both partners are carrying that weight individually, it doesn't take much to turn a shared dinner into a tribunal.

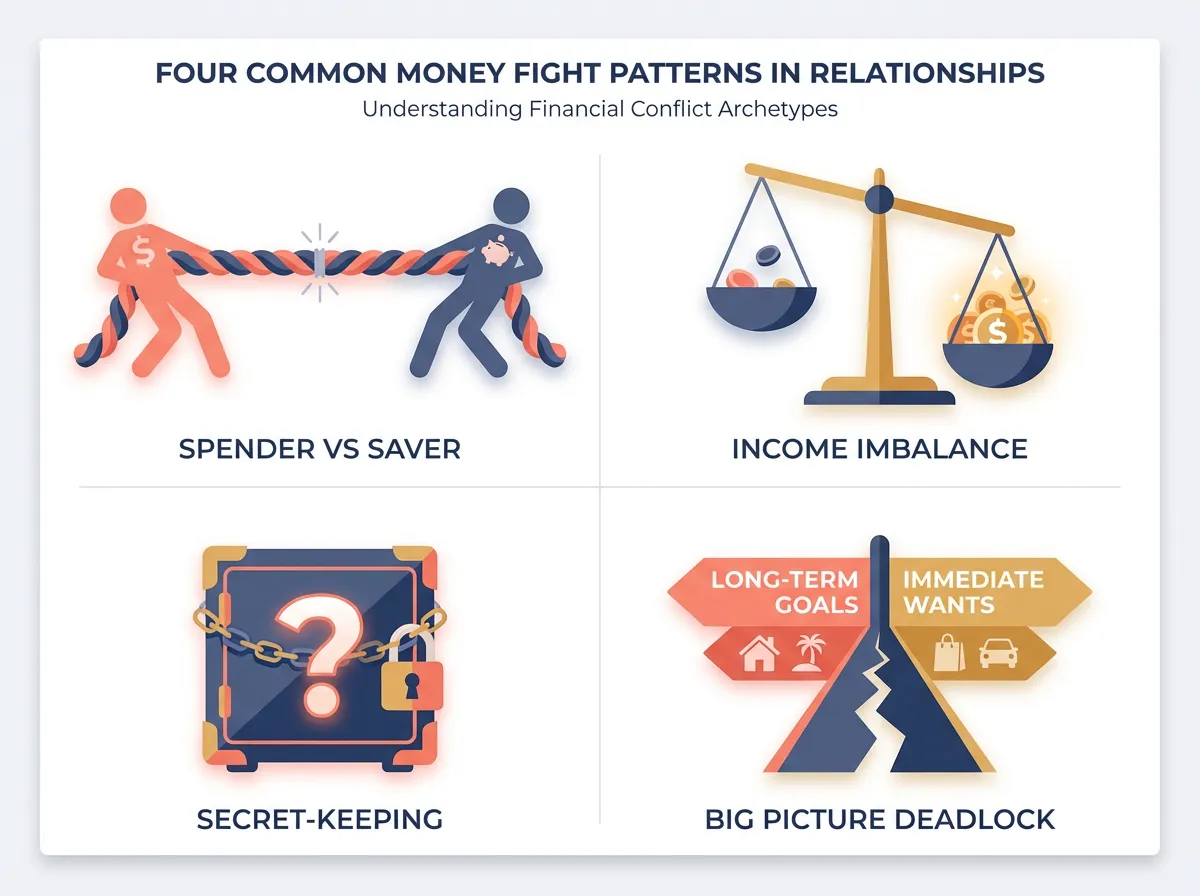

The 4 Money Fight Patterns (And What's Really Going On)

Not all money fights look the same. Identifying your pattern is the first step toward dismantling it.

1. The Spender vs. Saver Standoff

What it looks like: One partner thinks the other is reckless. The other feels controlled and micromanaged.

What's really happening: This is usually a clash of underlying money philosophies. The "spender" often views money as a tool for enjoying life now — perhaps because they grew up without much and want to make the most of what they have. The "saver" views money as a shield against future disaster — perhaps because they experienced financial instability as a child.

Neither is wrong. But when both partners believe their approach is the only responsible one, every purchase becomes a moral judgment.

Example: Priya and James fought constantly about dining out. James saw their weekly restaurant meals as the one thing that made their grueling work schedules bearable. Priya saw each receipt as evidence they'd never afford a house. Neither was being irrational — they were just measuring "responsible" against completely different yardsticks.

2. The Income Imbalance Power Struggle

What it looks like: The higher earner (consciously or not) acts as the final decision-maker. The lower earner feels dismissed or guilty for spending.

What's really happening: Income differences create an unspoken hierarchy that contradicts the partnership both people signed up for. The higher earner may not even realize they're wielding their income as authority. The lower earner may withdraw from financial conversations entirely, which only deepens the imbalance.

3. The Secret-Keeping Spiral

What it looks like: Hidden purchases, undisclosed debt, secret accounts.

What's really happening: Financial infidelity — and yes, that's the clinical term — usually isn't about deception for its own sake. It's a symptom of an environment where one or both partners feel they can't be honest about money without facing judgment or conflict. The hiding creates more shame, which creates more hiding.

4. The "Big Picture" Deadlock

What it looks like: One partner wants to invest aggressively; the other wants to pay off debt. One wants to relocate for a cheaper cost of living; the other won't leave their community.

What's really happening: You haven't aligned on what you're actually building together. Without a shared vision, every financial decision feels like a tug-of-war rather than a step forward.

How to Stop Fighting About Money (Without Pretending It Doesn't Matter)

Let's get practical. These aren't vague suggestions — they're specific, structured approaches that work even when emotions are running high.

Step 1: Have the "Money Story" Conversation

Before you ever open a spreadsheet together, sit down and ask each other these questions:

- What did money look like in your family growing up? Was it abundant? Scarce? A source of conflict between your parents?

- What's your biggest financial fear? Not having enough to retire? Being controlled? Missing out on life?

- When you imagine feeling "financially safe," what does that look like? A specific number in savings? Owning a home? Simply not worrying?

This conversation isn't about solving anything. It's about understanding the emotional operating system that drives your partner's financial behavior. When Priya learned that James's family rarely ate meals together and restaurants represented connection, not waste, the dynamic shifted entirely.

Step 2: Schedule a Weekly "Money Date"

The single most effective habit couples can adopt is a brief, recurring financial check-in. Here's a structure that works:

- When: Same day, same time, every week. Treat it like an appointment.

- Duration: 20 minutes. Set a timer. This prevents spiraling.

- Agenda:

- Review the past week's spending (no judgment, just awareness)

- Flag any upcoming expenses

- Check progress on one shared goal

- Each person shares one financial "win" from the week, no matter how small

Critical rule: This is the only time you discuss money during the week (except genuine emergencies). This eliminates the ambush dynamic — no more bringing up the credit card statement while your partner is cooking dinner.

Step 3: Build a "Yours, Mine, Ours" System

The all-or-nothing approach to joint finances breeds resentment. A three-account structure gives both partners autonomy and accountability:

- Joint account ("Ours"): Covers shared expenses — rent/mortgage, groceries, utilities, kids, shared savings goals. Both partners contribute a proportional percentage of their income (not a flat dollar amount — this matters for income-imbalanced couples).

- Individual accounts ("Yours" and "Mine"): Each partner gets a set amount of personal spending money, no questions asked. This is the pressure valve that prevents the "permission to buy" dynamic.

The specific amounts matter less than the principle: nobody should have to justify buying a book, a coffee, or a new shirt. Autonomy within structure prevents the small resentments that compound into blowups.

Step 4: Create Spending Thresholds — In Writing

"We should talk about big purchases" is vague enough to be useless. Instead, agree on a specific number:

- Under $75: No discussion needed. Spend from personal or joint as appropriate.

- $75–$300: Mention it to your partner (a text is fine). Not asking permission — just a heads-up.

- Over $300: Discuss before purchasing. Both partners agree.

Adjust the thresholds to your income. The magic isn't in the numbers — it's in having a clear, shared framework so neither person has to guess whether they're crossing a line. Consider formalizing agreements like these with a tool like Servanda, which helps couples create written, structured agreements that prevent the same conflicts from resurfacing.

Step 5: Fight the Problem, Not Each Other

When external financial pressure hits — a job loss, a medical bill, an interest rate hike — the instinct is to turn on each other. If you hadn't bought that car. If you'd taken that promotion. If we'd saved more.

Reframe the language:

- Instead of: "You spent too much this month."

-

Try: "We're over budget this month. What can we adjust?"

-

Instead of: "You never stick to the plan."

- Try: "The plan isn't working for us. Can we redesign it together?"

This isn't just semantics. The shift from "you vs. me" to "us vs. the problem" changes the neurological response. Your partner stops being a threat and starts being a teammate.

When Money Fights Are a Symptom of Something Bigger

Sometimes the money conflict is genuinely just about money — you need a budget and a system. But sometimes, persistent money fights are a surface expression of deeper relational issues:

- Control dynamics: One partner uses money to maintain power in the relationship.

- Unprocessed resentment: The money fight is a safe container for anger that's actually about something else entirely — feeling unsupported, disconnected, or taken for granted.

- Financial abuse: One partner deliberately restricts the other's access to money, monitors all spending, or weaponizes economic dependence. This is not a conflict to "resolve" — it's a pattern to escape.

If your money fights feel disproportionately intense, if they always end in the same painful place regardless of the topic, or if one partner consistently shuts down or becomes afraid during financial discussions, a couples therapist who specializes in financial conflict can help you identify whether you're dealing with a communication gap or something more structural.

A Note on Shame

Many couples avoid money conversations not because they're angry, but because they're ashamed. Ashamed of debt. Ashamed of not earning enough. Ashamed of not understanding investments or taxes or credit scores.

Shame thrives in silence. The antidote isn't a perfectly optimized budget — it's a partner who says, "We're in this together, and I'm not going to judge you for where we are. I only care about where we're going."

If you can offer that to each other, you've already won the hardest part of the fight.

Frequently Asked Questions

How do couples stop fighting about money?

The most effective approach is creating a structured system — scheduled money conversations, clear spending thresholds, and a shared-but-flexible account structure. Most money fights happen because of ambiguity and surprise, not fundamental disagreement. Remove those two triggers, and the frequency of fights drops dramatically.

Is it normal for couples to argue about finances?

Absolutely. Money is consistently ranked among the top three sources of conflict for couples at every income level. The issue isn't that you argue about money — it's whether those arguments lead to understanding and solutions or just repeat the same painful cycle.

Should couples combine all their finances?

There's no single right answer. Fully merged, fully separate, and hybrid systems can all work. The key is that both partners feel the system is fair and that neither person feels financially controlled or excluded. Many financial therapists recommend the "yours, mine, ours" three-account model as a starting point.

How do you talk to your partner about money without starting a fight?

Timing and framing matter enormously. Never bring up money when either of you is tired, hungry, or already stressed. Use a scheduled check-in so neither person feels ambushed. Start with curiosity ("I noticed our electric bill jumped — do you know what happened?") rather than accusation ("Why is the electric bill so high?").

Can financial disagreements cause divorce?

They can — and frequently do. Research from Kansas State University found that money arguments are the strongest predictor of divorce across income levels. However, it's not the disagreement itself that causes the split; it's the inability to work through the disagreement constructively. Couples who develop shared financial systems and address the emotional roots of their money conflicts significantly reduce this risk.

Moving Forward Together

Money fights feel uniquely personal because money touches every part of your shared life — where you live, how you eat, what future you can build, and how safe you feel getting there. But the couples who thrive financially aren't the ones who never disagree. They're the ones who've built a framework that turns disagreement into a design conversation instead of a courtroom.

Start small. Have the money story conversation this week. Schedule your first 20-minute money date. Agree on one spending threshold. You don't need to overhaul your entire financial life tonight — you just need to take the first step in the same direction.

The goal was never to stop caring about money. It was to stop letting money convince you that you're on opposite sides.