Why You Really Fight About Money (It's Not Money)

It's 9:47 PM on a Tuesday. One of you opens the credit card statement. The other notices a charge—maybe it's a $180 pair of running shoes, maybe it's another subscription service nobody asked about. Within sixty seconds, the kitchen is a courtroom. "You always do this." "You never let me enjoy anything." The argument ends the way it always does: someone retreats to another room, nothing gets resolved, and both of you feel misunderstood.

Sound familiar? Money is the number one topic couples fight about, and research consistently shows that financial disagreements are a stronger predictor of divorce than arguments about household chores, intimacy, or in-laws. But here's what most advice columns get wrong: the fight isn't really about the shoes, the subscription, or even the bank balance. The reason couples fight about money is because money is a proxy—a stand-in for safety, freedom, control, identity, and the invisible rules each of you absorbed long before you ever shared a checking account.

This article is going to take you beneath the spreadsheet.

Key Takeaways

- Money arguments are rarely about the dollar amount. They're driven by deeper needs like security, autonomy, and self-worth that each partner learned in childhood.

- Your family of origin gave you an unspoken "money script." Identifying yours—and your partner's—is the single most clarifying step you can take.

- Spenders and savers aren't opponents. They're two nervous systems responding to different childhood wounds, and understanding this reframes everything.

- You don't need to agree on every purchase. You need to agree on what money means in your shared life—and build rituals around that meaning.

- One structured conversation can replace months of silent resentment. This article gives you a framework to have it tonight.

The Real Reason Couples Fight About Money

Let's get the obvious out of the way: yes, financial stress is real. When there isn't enough money to cover rent, the argument has a material dimension that no amount of introspection will fix. But even couples with comfortable incomes fight about money with startling regularity. A 2022 study from the American Psychological Association found that 73% of adults reported money as a significant source of stress—and among partnered adults, the stress almost always became relational.

Why? Because money is never just money. Money is the answer to questions like:

- Am I safe?

- Am I free?

- Am I worthy?

- Do I have control over my own life?

- Will I end up like my parents?

When your partner challenges a financial decision, they aren't just questioning the purchase. They're—often unknowingly—poking at the raw nerve behind one of those questions. And when you react defensively, you're not defending the $180 shoes. You're defending your right to feel like a competent, autonomous adult.

This is why budgeting apps don't fix money fights. You can't spreadsheet your way out of an identity crisis.

Your Money Script: The Invisible Rulebook You Never Chose

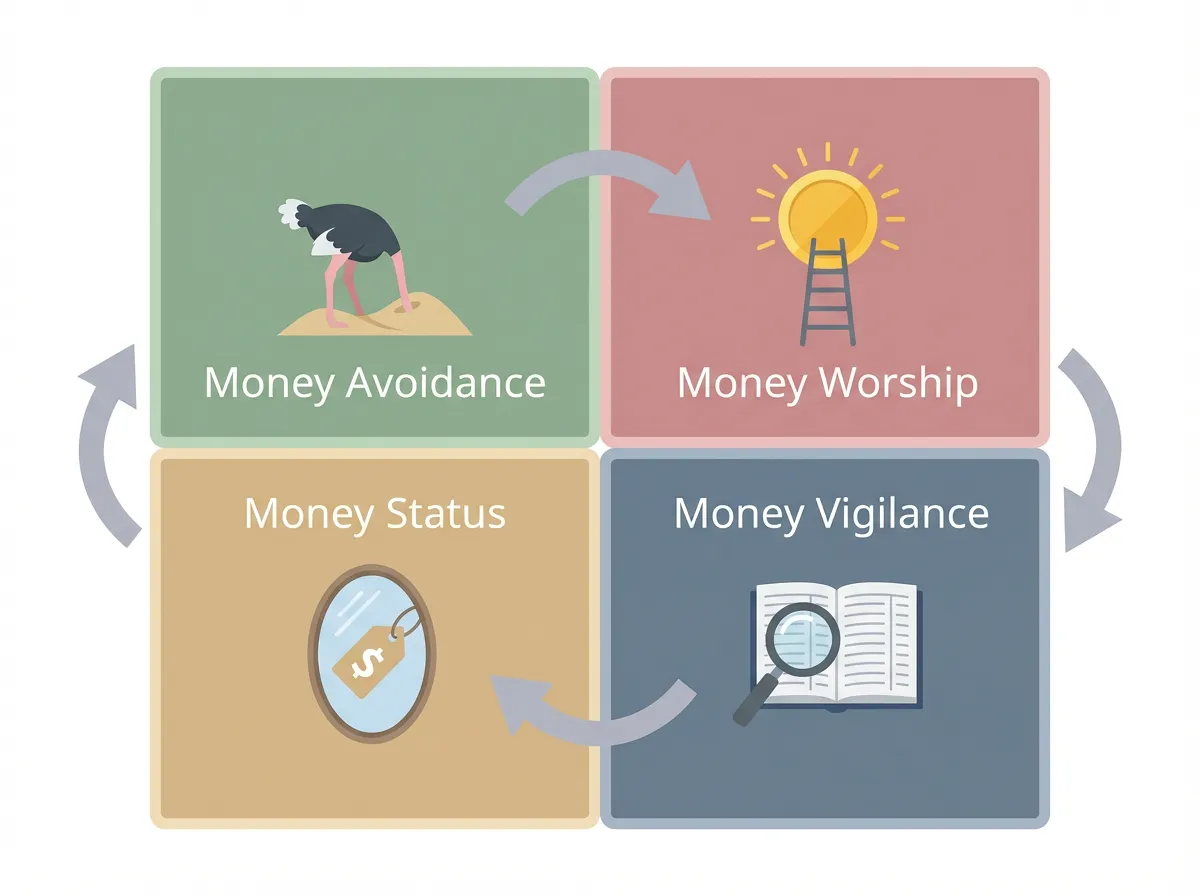

Financial psychologist Dr. Brad Klontz coined the term "money scripts"—the unconscious beliefs about money that form in childhood and operate on autopilot in adulthood. These scripts are absorbed, not taught. They come from watching, not listening.

Here are four common money scripts and the childhood experiences that tend to produce them:

1. Money Avoidance

The belief: Money is bad, or rich people are greedy, or I don't deserve financial comfort.

Childhood root: Growing up in a household where money was associated with conflict, guilt, or moral judgment. Maybe your parents fought bitterly about finances, so you learned that engaging with money at all was dangerous.

How it shows up in your relationship: You avoid looking at bank statements. You feel guilty about earning more than your partner. You defer all financial decisions, which your partner interprets as irresponsibility.

2. Money Worship

The belief: More money will solve everything. Happiness is just one raise away.

Childhood root: Growing up with scarcity—not necessarily poverty, but the feeling that there was never quite enough. Maybe your parents worked constantly, and you internalized the message that earning was the highest priority.

How it shows up in your relationship: You work long hours and resent your partner for not doing the same. You measure progress in net worth. When your partner wants to spend on experiences or leisure, you feel anxious.

3. Money Status

The belief: Self-worth equals net worth. You are what you own.

Childhood root: A household where appearances mattered. Maybe your family drove cars they couldn't afford or talked about neighbors in terms of what they had. Maybe love felt conditional on achievement.

How it shows up in your relationship: You overspend to project success. You feel ashamed of frugal choices. When your partner suggests cutting back, it feels like they're saying you're not enough.

4. Money Vigilance

The belief: You must be constantly watchful. Waste is a moral failing. Save for the worst, because the worst is always coming.

Childhood root: A household shaped by economic trauma—a parent who lost a job, a grandparent who survived the Depression, or a family that experienced a sudden financial shock.

How it shows up in your relationship: You monitor every expense. You feel physically uncomfortable when your partner spends spontaneously. You have trouble enjoying what you have because you're always bracing for loss.

Here's the critical insight: most couples are a collision of two different scripts. A money-avoidant partner paired with a money-vigilant one. A money-worshipper married to a money-status seeker. The fight isn't about the credit card bill. It's about two people operating from two invisible rulebooks, each convinced their rules are just "common sense."

What the Fight Is Actually About: Five Hidden Layers

Once you understand money scripts, you can start decoding what's really happening during a financial argument. Here are the five most common hidden layers beneath money fights:

Layer 1: Safety vs. Freedom

One partner needs a financial cushion to feel emotionally regulated. The other needs the ability to spend without permission to feel like an adult. Neither need is wrong. But when they collide, it feels like the other person is either controlling or reckless.

Layer 2: Trust and Transparency

Secret purchases, hidden accounts, "financial infidelity"—these aren't really about money. They're about the same thing all infidelity is about: the pain of discovering your partner has a private life that excludes you.

Layer 3: Power and Equality

In relationships where one partner earns significantly more, money can become a silent scoreboard. The higher earner may feel entitled to more decision-making power. The lower earner may feel dependent and resentful. Neither person created this dynamic on purpose—it's baked into cultural narratives about who "earns" authority.

Layer 4: Parenting Ghosts

You're not just arguing with your partner. You're arguing with your father who called your mother wasteful. You're arguing with your mother who hid grocery receipts. You're arguing with the version of yourself who swore, at age twelve, I'll never let this happen to me.

Layer 5: Competing Visions of the Future

Every financial decision is a vote for a certain kind of future. When your partner wants to save aggressively, they're voting for security. When you want to travel now, you're voting for richness of experience. The fight breaks out when neither of you has made these visions explicit.

How to Actually Talk About Money (Without It Becoming a Fight)

Forget the advice to "sit down and make a budget together." That's like telling someone with a fear of flying to just read the safety card. The issue isn't information. It's emotion. Here's a different approach:

Step 1: Map Your Money Origin Story

Separately, each of you writes down answers to these questions:

- What's your earliest memory involving money?

- What did your parents fight about financially?

- What was the unspoken rule about money in your household?

- When you spend money, what feeling are you chasing?

- When you save money, what fear are you managing?

Then share—not to debate, but to listen. The goal is curiosity, not correction.

Step 2: Name Your Scripts Without Judgment

Using the four categories above (avoidance, worship, status, vigilance), identify your dominant script and your partner's. Say it out loud: "I think I'm mostly money-vigilant because my dad lost his business when I was ten, and I've been terrified of financial instability ever since."

This single act of naming transforms the dynamic. Suddenly your partner isn't "controlling"—they're scared. You're not "irresponsible"—you're trying to feel alive.

Step 3: Identify the Trigger, Not the Topic

Next time a money argument starts, pause and ask: "What just got activated in me?" Not "who's right about whether we can afford this," but "why does my chest feel tight right now?"

Some examples:

- "When you questioned that purchase, I felt like a child being scolded."

- "When I saw that charge, I felt the same panic I felt when my mom couldn't pay our electric bill."

This is vulnerable. It's supposed to be. Vulnerability is the only thing that actually interrupts the cycle.

Step 4: Create Money Rituals, Not Rules

Rules feel like control. Rituals feel like partnership. The difference is consent and shared meaning.

Instead of: "We need to approve any purchase over $100." Try: "Let's have a weekly 15-minute money check-in on Sunday mornings with coffee. We each share one thing we spent on that felt good and one thing that felt stressful."

Instead of: "We need separate accounts." Try: "Let's each have a 'no-questions-asked' fund—an amount we agree on that either of us can spend freely, so neither of us feels monitored."

The structure matters less than the spirit. The point is building a shared financial culture that honors both scripts.

Step 5: Write It Down

Verbal agreements made during emotional conversations have a short shelf life. When you reach a genuine understanding—about spending thresholds, savings goals, or how you'll handle financial stress—write it down. Not as a legal contract, but as a shared document you can return to when emotions flare. Tools like Servanda can help couples formalize these agreements in a structured way, so you're not relying on memory during your next tense moment.

When It's Bigger Than a Conversation

Some money conflicts have roots that a Sunday morning check-in can't reach. If any of these apply, consider working with a financial therapist (yes, that's a real specialty):

- One or both of you grew up in poverty or financial chaos

- There's active financial deception in the relationship

- Money arguments routinely escalate to yelling, stonewalling, or threats

- One partner controls all financial access and the other has none

- Debt has become a source of shame that prevents honest conversation

Financial therapy combines traditional couples therapy with financial planning—addressing the emotional roots and the practical realities simultaneously. It's not a sign of failure. It's a sign you're taking the problem seriously enough to get expert help.

A Quick Self-Assessment: What's Your Money Conflict Style?

Answer honestly:

-

When your partner makes a purchase you didn't expect, your first instinct is: - (a) Anxiety — What if we need that money later? - (b) Hurt — Why didn't they tell me? - (c) Anger — They don't respect our goals. - (d) Nothing — I'd rather not think about it.

-

When you think about your financial future, the dominant emotion is: - (a) Fear - (b) Hope - (c) Determination - (d) Numbness

-

The phrase that best describes your parents' relationship with money: - (a) Tense and secretive - (b) Generous but chaotic - (c) Disciplined and rigid - (d) We didn't talk about it

There's no score. The point is to notice your patterns—and to share your answers with your partner as a conversation starter, not a diagnosis.

FAQ

Is it normal for couples to fight about money?

Absolutely. Financial disagreements are the most common source of recurring conflict for couples across income levels, according to multiple studies. The frequency of the fights isn't the problem—the problem is when the same argument keeps replaying without either partner understanding what's driving it beneath the surface.

How do you stop arguing about money with your partner?

You stop by changing what you argue about. Instead of debating the purchase itself, explore the feelings and childhood patterns underneath it. The steps in this article—mapping your money origin story, naming your money scripts, and building shared rituals—give you a way to have productive financial conversations instead of reactive ones.

What are money scripts and how do they affect relationships?

Money scripts are unconscious beliefs about money that form in childhood, identified by financial psychologist Dr. Brad Klontz. They fall into four categories: avoidance, worship, status, and vigilance. They affect relationships because each partner operates from a different script, creating clashes that feel like value conflicts but are actually unexamined childhood patterns.

Should couples have joint or separate bank accounts?

There's no universally right answer. The real question is: what arrangement allows both partners to feel safe and autonomous? Many couples find a hybrid works best—a shared account for joint expenses and individual accounts for personal spending. The arrangement itself matters less than whether both people genuinely agreed to it.

When should couples see a financial therapist?

Consider it when money arguments have become cyclical, emotionally intense, or involve secrecy and shame. Financial therapists are trained to address both the emotional patterns and the practical financial decisions simultaneously—something that a regular couples therapist or financial planner alone may not cover.

Moving Forward Together

The most important thing to understand about money fights is that they're not evidence that your relationship is broken. They're evidence that two people with two different histories are trying to build one shared life—and that's genuinely hard.

You don't need to agree on every purchase. You don't need identical money scripts. You need to understand where your partner's reactions come from, share where yours come from, and build a financial life together that respects both histories instead of erasing one.

The next time a credit card statement threatens to ruin your evening, try this: instead of asking "Why did you spend that?" ask "What were you feeling when you bought that?" It's a small question. It changes everything.

Your money story started before your relationship did. But how it ends? That part you write together.